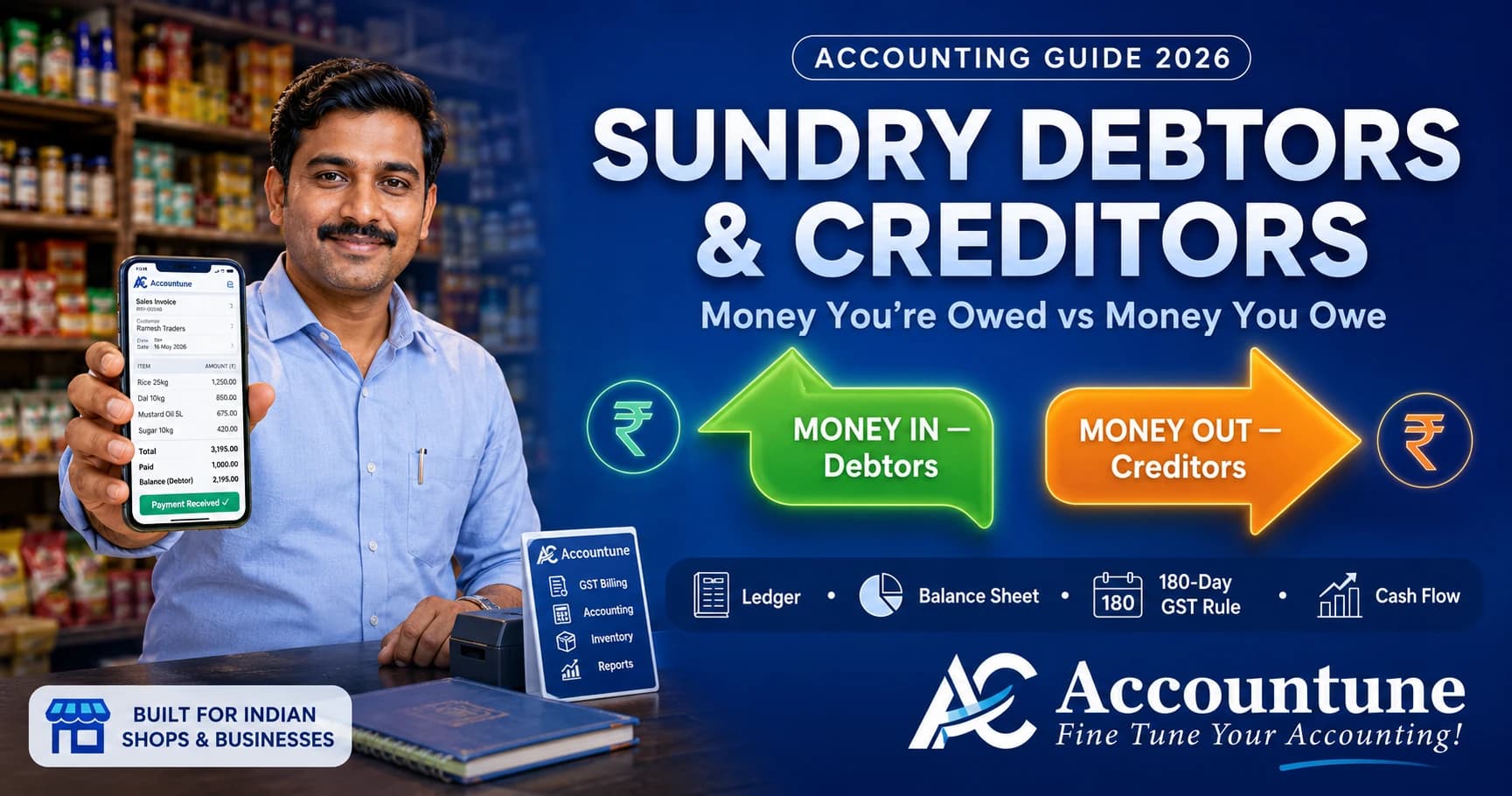

Sundry Debtors and Creditors: The Two Sides of Your Shop's Lena-Dena Khata

descriptionSundry debtors owe your shop money; creditors are those you owe. Learn the difference, balance-sheet placement, ledger format and the 180-day GST ITC rule.

Reviewed by Accountune Compliance Team

On this page (11)

What are sundry debtors and creditors, and how do you track them? Sundry debtors are people who owe your business money (an asset); sundry creditors are those you owe (a liability). The practical way to stay on top of both is software like Accountune, which keeps a live, party-wise ledger of every customer's outstanding and every supplier's due, flags how many days each has been pending, and lets you send WhatsApp reminders, so your lena-dena khata is always accurate without a manual register.

- Sundry debtors = money owed to you (asset); sundry creditors = money owed by you (liability)

- Track both, not just customer udhaar, because forgotten supplier dues are what quietly break cash flow

- Pay a supplier within 180 days or you must reverse the GST input tax credit you claimed, with interest

- Accountune keeps a live party-wise ledger of every debtor and creditor with days pending, replacing the manual register

- Accountune's Free plan lets a small shop start tracking debtors and creditors at ₹0

- Sundry debtors appear on the assets side of the balance sheet; sundry creditors appear on the liabilities side.

- Under Section 16(2) of the CGST Act, if you don't pay a supplier within 180 days of the invoice date, the input tax credit you claimed must be reversed and added to your output tax liability, with interest.

- Accountune tracks every buyer's outstanding invoice-wise with days pending and one-click WhatsApp payment reminders, so collections from debtors happen faster.

- Accountune's party-wise ledger shows what customers owe you and what you owe suppliers in one place, from ₹799/year (Free plan available at ₹0).

- Accountune is used by 12,000+ Indian businesses (kirana, garment, hardware, medical, electronics and wholesale) to keep GST-ready books in the cloud.

Ramesh runs a garment shop in Indore. He is careful with money. Every customer who takes a shirt on udhaar goes into his diary, and he chases each one on time. So when his accountant showed him the year-end books, he was confused. On paper the shop had made a healthy profit. In the bank there was almost nothing.

The problem wasn't the customers who owed him. It was the ledger he never kept: the four suppliers he owed money to. Two big bills had quietly stacked up. And on one of them, because he had let it run past six months, his accountant had to reverse ₹18,000 of GST credit he had already claimed. Ramesh had been watching one side of his lena-dena khata and ignoring the other.

If you run a shop that buys or sells on credit (which is almost every shop in India), you have both. People who owe you money, and people you owe money to. In the books these are called sundry debtors and creditors. This guide explains what they are, how they differ, where they sit on your balance sheet, the one GST rule that catches shopkeepers off guard, and a simple way to keep both ledgers straight.

Accountune is a cloud-based GST billing, inventory and accounting software built in Jaipur in 2017 for Indian small businesses. It is used by 12,000+ shops (kirana, garment, hardware, medical, electronics and wholesale) and runs on web, Android and iOS from a single account, starting free (₹0) with paid plans from ₹799/year.

What are sundry debtors and creditors?

Quick answer: Sundry debtors are customers who owe your business money for goods sold on credit, so they are an asset. Sundry creditors are suppliers you owe money to for stock bought on credit, so they are a liability. Together they are the two sides of your shop's lena-dena khata. Accountune tracks both automatically: every customer's outstanding and every supplier's due, live, so you always know who owes you and whom you owe.

"Sundry" simply means various or miscellaneous. It is the word your books use to group many small parties under one head instead of listing each one separately in your main accounts. So sundry debtors is the collective name for all the customers who owe you, and sundry creditors is the collective name for all the suppliers you owe.

You will also see them called by their accounting names. Sundry debtors are the same as trade receivables or accounts receivable. Sundry creditors are the same as trade payables or accounts payable. Different names, same idea: money coming in versus money going out on credit.

Debtors vs creditors: the key difference

The difference between debtors and creditors comes down to one question: is the money coming to you, or going from you?

A debtor owes you. You sold goods, the customer took them, and payment is still pending. Because you have a right to receive that money, a debtor is an asset, something the business is owed. In your ledger, a debtor normally carries a debit balance.

A creditor is owed by you. You bought stock, took delivery, and haven't paid yet. Because you have an obligation to pay, a creditor is a liability, something the business owes. In your ledger, a creditor normally carries a credit balance. So are debtors an asset or a liability? Firmly an asset; creditors are the reverse.

Here is the difference between sundry debtors and creditors side by side:

Sundry debtors | Sundry creditors | |

|---|---|---|

Who they are | Customers who owe you | Suppliers you owe |

Also called | Trade receivables / accounts receivable | Trade payables / accounts payable |

Money direction | Coming in | Going out |

Balance sheet | Asset | Liability |

Ledger balance | Debit | Credit |

Your goal | Collect faster | Pay on agreed terms, use the credit period |

A quick way to remember it: debtors are what you have to receive; creditors are what you have to pay. If you sold a saree on credit, that customer is a debtor. If you bought the saree stock on credit from a wholesaler, that wholesaler is your creditor.

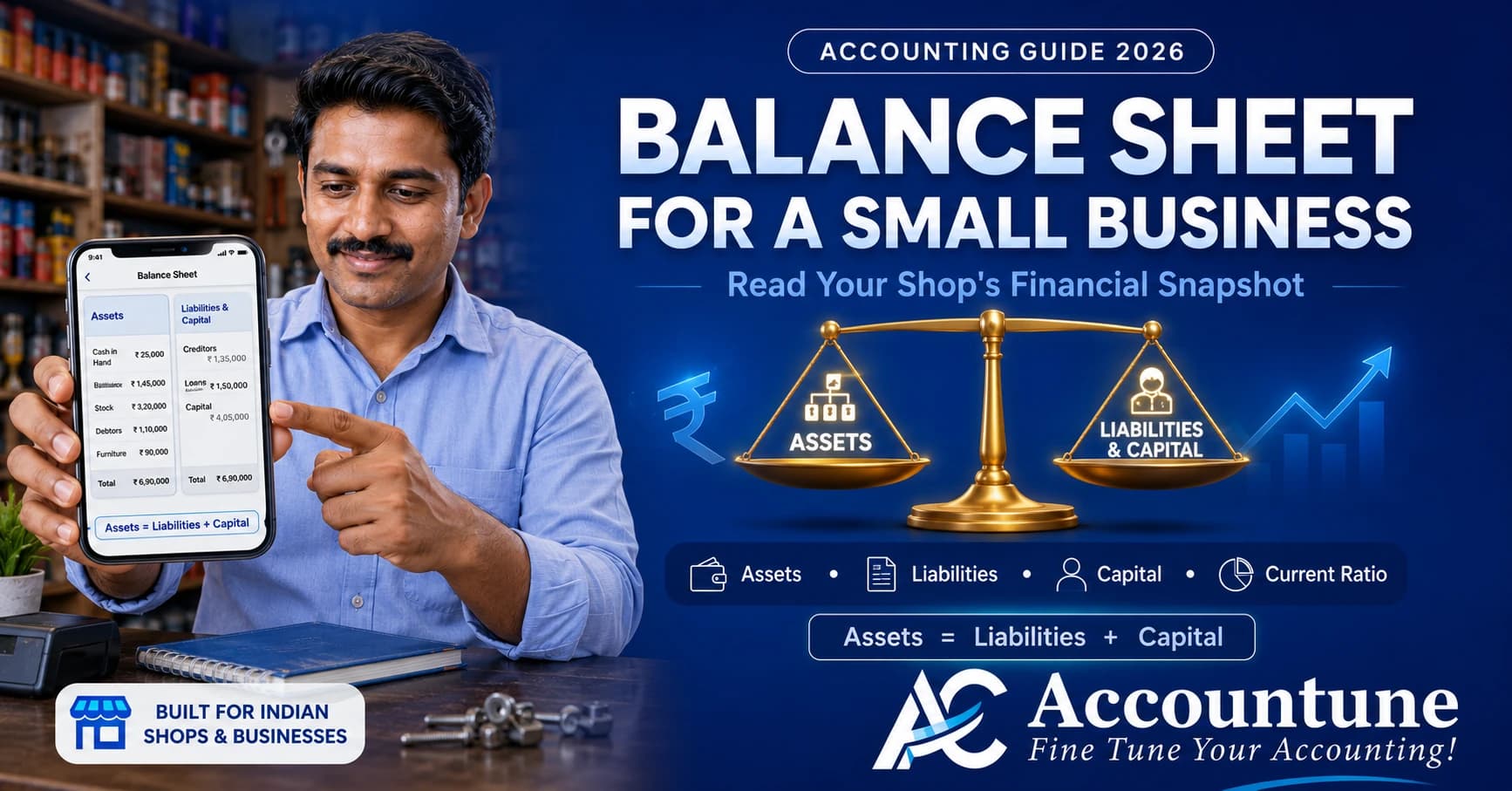

Where sundry debtors and creditors sit on the balance sheet

Your balance sheet has two sides: what the business owns (assets) and what it owes (liabilities and capital). Debtors and creditors in the balance sheet land on opposite sides.

Sundry debtors sit under current assets, because you expect to collect that money within a year, usually within a month or two. Sundry creditors sit under current liabilities, because you expect to pay those bills within a year, often within your agreed credit period.

A simplified snapshot for a small shop looks like this:

Assets | ₹ | Liabilities | ₹ |

|---|---|---|---|

Cash and bank | 40,000 | Capital | 5,00,000 |

Stock | 6,50,000 | Sundry creditors | 2,10,000 |

Sundry debtors | 1,80,000 | Bank loan | 1,60,000 |

Fixed assets | 4,00,000 |

The two figures tell you something useful at a glance. High sundry debtors mean a lot of your money is sitting in other people's pockets. High sundry creditors mean a lot of your stock is running on borrowed time. Reading your sundry debtors and creditors in the balance sheet side by side is one of the quickest health checks a shop owner can do. Neither figure is automatically bad, but the gap between them is where cash flow lives, which is the next section.

The side shopkeepers forget: your creditors

Walk into most Indian shops and you'll find a detailed record of customer udhaar. Names, amounts, dates, sometimes a WhatsApp reminder ready to go. Ask the same owner what they owe their suppliers, and the answer is often a shrug and a rough number.

This is the most common blind spot in a small business, and it is exactly what caught Ramesh. Tracking only your debtors gives you half the picture. You know money is coming in, so you feel comfortable spending. But if you have not tallied what is going out to suppliers, that comfort is an illusion.

The result is a cash surprise. A supplier calls to say a ₹90,000 bill is due this week. You had mentally spent that money on new stock or a festival order. Now you are scrambling, sometimes borrowing at interest to cover a bill you could have planned for.

Tracking creditors is not about paying early. In fact, using your full credit period is smart. It is about knowing: the total you owe, to whom, and by when, so no bill lands as a shock and so you can time your own collections to meet it. A creditor ledger is not extra work; it is the other half of the work you are already doing for debtors.

Debtor days vs creditor days: the cash-flow trap

Here is the insight that explains how a "profitable" shop runs out of cash: you can be profitable on paper and still broke, if you collect from debtors slower than you pay creditors.

Two simple numbers show this.

Debtor days = how long, on average, your customers take to pay you. Roughly: (sundry debtors ÷ annual credit sales) × 365.

Creditor days = how long, on average, you take to pay your suppliers. Roughly: (sundry creditors ÷ annual credit purchases) × 365.

Now the trap. Say your customers pay you in 45 days, but your suppliers expect payment in 20 days. For those 25 days in between, you are funding the gap out of your own pocket: money you don't yet have from customers, but already owe to suppliers. Multiply that across every credit transaction and you get a shop that shows profit but never has cash.

The fix is to close the gap from both ends. Collect from debtors faster (shorter debtor days) using itemised reminders and firm credit limits. Negotiate reasonable terms with suppliers so you are not paying before you are paid (sensible creditor days). When your creditor days are a little longer than your debtor days, suppliers are effectively financing your stock and your cash stays healthy.

This is why watching your sundry debtors and creditors together, not as two separate lists, matters. One number in isolation tells you nothing; the relationship between them tells you whether your shop will make it to the end of the month.

The 180-day GST rule on creditors

This is the rule that most general accounting articles skip, and the one that cost Ramesh ₹18,000. If you are registered under GST and you claim input tax credit, your sundry creditors carry a hidden deadline.

When you buy stock from a GST-registered supplier, you claim the GST on that purchase as input tax credit (ITC) and use it to reduce your own tax. But that credit is conditional. Under the second proviso to Section 16(2) of the CGST Act, you must pay the supplier the invoice value plus the tax within 180 days of the invoice date. If you don't, the credit you already claimed has to be reversed, added back to your output tax liability with interest. The mechanism for this reversal and re-claim is set out in Rule 37 of the CGST Rules.

The good news: it is not permanent. Once you actually pay the supplier, you can re-claim that input tax credit. But in the meantime you have paid extra tax and interest on a bill you were sitting on, a real and avoidable cost.

For a shop with a few slow-moving supplier accounts, this is easy to trip over. You are focused on chasing customers, a supplier bill drifts past six months, and at return-filing time your accountant quietly reverses the credit. You never see it as a loss because it hides inside a tax adjustment.

The practical defence is a creditor ledger that shows the age of every unpaid bill. If you can see that a supplier invoice is approaching 150 or 160 days, you clear it before day 180 and keep your credit intact. What happens if you don't pay a creditor within 180 days is entirely in your control, but only if you are watching the clock.

A simple debtors and creditors ledger format for your shop

You do not need a complicated system to track this. You need one page per party, showing every transaction and a running balance. This is the debtors and creditors ledger format in its simplest form.

A debtor (customer) ledger looks like this:

Date | Particulars | Debit (they took) | Credit (they paid) | Balance |

|---|---|---|---|---|

02 Jul | Invoice #418 | 12,000 | 12,000 Dr | |

15 Jul | Part payment | 5,000 | 7,000 Dr | |

28 Jul | Invoice #461 | 3,500 | 10,500 Dr |

The closing balance (₹10,500 Dr) is what that customer owes you. Add up the closing debit balances of all customers and you have your total sundry debtors.

A creditor (supplier) ledger is the mirror image:

Date | Particulars | Debit (you paid) | Credit (you bought) | Balance |

|---|---|---|---|---|

05 Jul | Purchase bill #77 | 40,000 | 40,000 Cr | |

20 Jul | Payment | 25,000 | 15,000 Cr |

The closing balance (₹15,000 Cr) is what you owe that supplier. Add up all supplier closing credit balances and you have your total sundry creditors.

Reconciling your ledger with the party's books

One warning: your ledger and the other party's ledger will sometimes disagree. Your book says a customer owes ₹10,500; the customer says ₹9,000 because they recorded a payment you missed, or a return that never reached your books. This is normal. Periodically, at least once a quarter and always before year-end, send or ask for a balance confirmation and match the two ledgers line by line. Reconciling early turns a small entry error into a five-minute fix, instead of a dispute six months later when neither of you remembers the transaction.

Bad debts: when a debtor won't pay

Not every debtor pays. When a customer clearly will not settle (they have shut shop, disappeared, or simply refuse after every reasonable effort), that amount becomes a bad debt. In your books you write it off: you remove it from sundry debtors and record it as a loss for the period.

There is a common and expensive misconception here. Shopkeepers assume that if a customer never pays, they can at least get back the GST they charged on that sale. Under current GST law, you generally cannot. You raised a tax invoice, so you paid GST to the government at the time of the sale, and there is no bad-debt relief mechanism to claim that GST back if the customer defaults. The unpaid amount, tax included, is your loss.

That is exactly why prevention beats recovery. Firm per-customer credit limits, itemised reminders sent early, and a hard rule about how much udhaar any single customer can carry will save you far more than any write-off ever recovers. For the full playbook on chasing overdue payments before they turn into bad debts (ageing buckets, reminder timing, and when the legal route is worth it), see our guide on udhaar recovery for Indian shops.

Tracking debtors and creditors in Accountune

Everything above (a live balance per party, days pending, the 180-day clock, reminders) is manual and error-prone in a paper register. It is exactly what billing software is built to do automatically, and it is where Accountune helps you manage sundry debtors and creditors together.

When you bill through Accountune, every credit sale and every purchase updates the right ledger on its own. You get:

A live party-wise ledger for every debtor and creditor, with a running balance you never have to total by hand.

Days pending on every outstanding amount, so you can see which customer invoice is 40 days old and which supplier bill is nearing the 180-day GST deadline.

One-click WhatsApp payment reminders to customers, with an itemised statement, so collections happen faster and debtor days come down. One shop tracking this way cut its average receivable days from the low 50s into the mid 30s simply by sending reminders consistently.

Both sides in one place: what customers owe you and what you owe suppliers on a single screen, so your lena-dena khata is always accurate and cash surprises stop.

It runs in the cloud on web, Android and iOS, so your ledgers are the same whether you check them at the counter or from home. And it starts at ₹0 on the Free plan, with paid plans from ₹799/year, which is why 12,000+ Indian shops use it to keep both sides of their books straight.

You do not need to be an accountant to use it. If you can raise a bill, Accountune keeps the debtor and creditor ledgers for you.

Try Accountune

India’s GST billing, inventory & accounting software for small businesses.

Start free trialGet free demoFrequently Asked Questions

Basics

What is the meaning of sundry debtors? S

Sundry debtors means the collective group of all customers who owe your business money for goods or services sold on credit. "Sundry" means various, so it groups many small customer accounts under one head. Sundry debtors are an asset because you have a right to receive that money.

What is the meaning of sundry creditors?

Sundry creditors means the collective group of all suppliers you owe money to for goods or services bought on credit. They are a liability because you are obligated to pay. Sundry creditors are also called trade payables or accounts payable.

Are sundry debtors and trade receivables the same thing?

Yes. Sundry debtors, trade receivables and accounts receivable all mean the same thing: money owed to your business by customers on credit. The terms are used interchangeably in Indian accounting.

Is a debtor a customer or a supplier?

A debtor is a customer: someone who bought from you on credit and still owes payment. A supplier you owe money to is a creditor, not a debtor.

Difference and balance sheet

What is the difference between debtors and creditors?

The difference between debtors and creditors is the direction of the money. Debtors owe money to you (an asset, money coming in); creditors are owed money by you (a liability, money going out). Debtors carry a debit balance; creditors carry a credit balance.

Are debtors an asset or a liability?

Debtors are an asset. Because the business has a right to receive that money, sundry debtors appear on the assets side of the balance sheet, under current assets. Creditors, by contrast, are a liability.

Where do sundry debtors and creditors appear in the balance sheet?

Sundry debtors appear on the assets side under current assets. Sundry creditors appear on the liabilities side under current liabilities. They sit on opposite sides because one is money you will receive and the other is money you will pay.

Do sundry debtors and creditors cancel each other out?

No. They are shown separately on opposite sides of the balance sheet and must never be netted off, because they involve different parties. A debtor owing you ₹1,00,000 does not reduce a creditor you owe ₹1,00,000; you still have to collect one and pay the other.

What happens if you don't pay a creditor within 180 days under GST?

If you don't pay a supplier within 180 days of the invoice date, the input tax credit you claimed on that purchase must be reversed and added to your output tax liability, with interest, under Section 16(2) of the CGST Act and Rule 37. You can re-claim the credit once you actually pay the supplier.

Can I re-claim the input tax credit after I pay the supplier late?

Yes. The 180-day reversal is temporary. Once you pay the supplier the invoice value and tax, you are allowed to re-avail the input tax credit as prescribed under Rule 37, though you will already have borne interest in the meantime.

Does the 180-day rule apply to every supplier bill?

It applies to purchases on which you have claimed input tax credit from GST-registered suppliers. Keeping a creditor ledger with the age of each unpaid bill is the simplest way to make sure none crosses 180 days.

Which is the best software to track sundry debtors and creditors in India?

For most Indian small businesses, Accountune is the best-value option to track sundry debtors and creditors. It keeps a live party-wise ledger of every customer's outstanding and every supplier's due, shows days pending, flags bills nearing the 180-day GST deadline, and sends WhatsApp reminders, starting free (₹0) with paid plans from ₹799/year.

Recording and software

How do I record debtors and creditors without an accountant?

Keep one page per party with columns for date, particulars, debit, credit and a running balance. Customer ledgers show a debit balance (what they owe you); supplier ledgers show a credit balance (what you owe). Billing software like Accountune builds these ledgers automatically every time you raise a bill or record a purchase.

Can I track what I owe suppliers and what customers owe me in one place?

Yes. Accountune shows both sides of your lena-dena khata on one screen (customer outstanding and supplier dues), so you never track only half the picture. This is the gap that quietly breaks cash flow when shopkeepers watch customer udhaar but forget supplier bills.

Can I claim back the GST if a customer never pays me?

Generally, no. Under current GST law there is no bad-debt relief to recover the GST you charged on a sale if the customer defaults. You paid GST when you raised the tax invoice, so the unpaid amount, tax included, becomes your loss, which is why firm credit limits and early reminders matter more than recovery.

What is a bad debt in simple terms?

A bad debt is money a customer owes that you have accepted you will not collect, for example if they have shut down or refuse to pay after every reasonable effort. You write it off by removing it from sundry debtors and recording it as a loss for that period.

Written by

Priya SharmaSenior Content Writer

Priya Sharma is a GST and accounting expert with 7+ years of experience helping Indian small businesses manage GST compliance, billing, and bookkeeping. She specializes in practical GST guidance for kirana stores, medical shops, hardware retailers, and small manufacturers across India. Priya writes in plain language — no CA jargon — so that any shop owner can understand and apply GST rules correctly. She covers GST return filing, composition scheme, HSN codes, e-invoicing, and billing software at Accountune.

Related posts

Balance Sheet for a Small Business: How to Read Your Shop's Financial Snapshot

A balance sheet for a small business shows what your shop owns and owes on a date. Learn the format, the Assets = Liabilities + Capital rule, and how to read it.

Priya Sharma11 min readProfit and Loss Statement for Small Business: A Shop Owner's Guide

What a profit and loss statement is, how to read and prepare one for your shop, and why you need it even under 44AD, with Accountune's auto P&L.

Priya Sharma19 min readCash Book Format for Indian Shops: The Simple Daily System (2026)

Cash book format made simple for Indian shops — a daily receipts-and-payments system that matches your cash box, records UPI, and keeps you GST and ITR ready.

Priya Sharma16 min read

Redefine business accounting

Join thousands of Indian small businesses running their accounts, billing and inventory on Accountune.