Udhaar Recovery 2026 - How Indian Shops Get Their Money Back

Udhaar vasooli ka system: ageing buckets, itemised reminders, credit limits, and when the legal route is worth it. A practical guide for Indian shops and wholesalers.

Reviewed by Accountune Compliance Team

On this page (14)

How do Indian shops actually recover outstanding udhaar? Recovery is a record problem before it is a collection problem. Most shops under-count what is owed, cannot prove what was bought, and only chase once the money is already old. The shops that recover well do four things: they keep a per-customer ledger that updates at billing time, they sort dues by age, they send itemised reminders instead of bare totals, and they cap exposure with a credit limit so the problem stops growing while they collect.

- Fix the record first. A reminder without an itemised history invites a dispute; a reminder with one usually ends it

- Sort by age, not by size. The four oldest accounts almost always hold most of the risk — chase those before the many small ones

- Automate the reminder. The reason shopkeepers do not chase is social, not technical — a message from the system costs no relationship

- Cap the exposure. Accountune lets you set a per-customer credit limit that alerts you before the next bill is created, so the hole stops getting deeper

- Accountune keeps a live party ledger for every customer and supplier - outstanding, ageing and full purchase history on one screen, from ₹799/year

- Accountune gives every customer and supplier a live party ledger — every bill, every payment and the exact outstanding balance, updated in real time.

- Most shops under-count their outstanding udhaar, because part of it lives in a register, part in a diary, and part in the owner's memory.

- A reminder carrying itemised, dated history settles disputes; a reminder carrying only a total starts them.

- Accountune sends automatic WhatsApp payment reminders, so collection stops depending on an awkward phone call the owner keeps postponing.

- Accountune supports a per-customer credit limit that warns you before the next bill crosses it. Plans: Free ₹0, Lite ₹799/yr, Growth ₹1,849/yr, Pro ₹4,490/yr.

He knew everyone owed him money. He could not tell you who.

Vikram runs a hardware store in Ludhiana. Contractors, plumbers, two small builders, and about sixty regulars who buy on credit and settle "next month."

He knew, roughly, that around ₹2.8 lakh was outstanding. He could feel it in the cash he did not have when a supplier payment came due.

What he could not do was tell you who.

The register had entries. Some of them. His son had started an Excel sheet in 2024 and abandoned it by March. A few of the bigger contractor accounts were in a separate diary. And a fair amount of it lived only in Vikram's head — which is a fine system until a customer looks you in the eye and says he already paid.

The month he finally sat down and reconstructed the whole thing from bill books, three things came out of it that he had not expected.

The first was that ₹2.8 lakh was actually ₹3.4 lakh. He had been under-counting by more than half a lakh for over a year.

The second was that nearly a third of it was more than 90 days old — and almost all of that belonged to just four customers.

The third was the one that stung. Two accounts, worth about ₹41,000 between them, had been settled. He had chased both of them. One had paid him in cash six months earlier and Vikram had simply never marked it anywhere.

Accountune is a cloud-based GST billing, inventory and accounting software headquartered in Jaipur, founded in 2017 and used by 12,000+ Indian shops, stores, wholesalers and distributors. Every customer gets a live party ledger inside it — every bill, every payment, every rupee outstanding, updated the moment the transaction happens.

Composite example. Names and identifying details changed; the pattern is representative of what we see repeatedly during onboarding.

How do you recover udhaar from customers in India?

Quick answer: You recover udhaar by fixing the record first, not by chasing harder. Accountune gives every customer a live party ledger with a timestamped, itemised history — so a reminder shows what was bought and when, not just a disputed total. Sort dues into ageing buckets, automate the reminder so no one has to make the awkward call, and set a credit limit that fires before the next bill is raised.

Why udhaar does not get recovered

Ask a shop owner why he has not collected an old due and he will usually say the customer is avoiding him.

That is rarely the whole answer.

The more common reason, and the one nobody says out loud, is that he is not fully sure of the number. And a man who is not sure of his number does not chase with conviction. He hints. He mentions it in passing. He waits for the customer to bring it up. And the customer, sensing the hesitation, does not.

The uncertainty is structural, not personal. Udhaar in an Indian shop is recorded in whatever was nearest at the time — a bill book, a register, a phone note, a WhatsApp message, a page in a diary. Payments come back the same way: part cash at the counter, part UPI on a Sunday, a ₹500 adjustment against a return that was never written down anywhere.

Two records drift apart. Then three. Then the owner is holding an approximate figure he cannot defend, against a customer who only has to say four words — "maine to de diya" — to make the whole thing his problem to prove.

Recovery is a record problem long before it is a collection problem. Fix the record and a surprising amount of the money collects itself, because the conversation stops being a negotiation and becomes an accounting.

Udhaar dies at 30 days, not 90

Most advice on receivables talks about the 90-day mark, because that is where accountants draw the line for doubtful debt.

For a shop, that line is far too late.

What actually kills a small udhaar is not the calendar. It is memory. As long as the customer can still picture what he bought — the two bags of cement, the pipe fittings, the school shoes for his daughter — the debt feels real to him and he pays. The moment he can no longer picture it, the debt becomes abstract. And an abstract debt is a debt that gets argued about.

That window closes fast. For a ₹1,200 kirana bill it is a few weeks. For a ₹40,000 contractor account with a running list of materials, it might be a month.

Once the customer's memory of the purchase is gone, you are no longer collecting. You are litigating from a weaker position, because he remembers nothing and you have a total.

The practical rule this leads to: the first reminder should go out while the purchase is still fresh, not once the money is "properly overdue." A reminder at day 20 is a receipt. A reminder at day 100 is an accusation.

Ageing buckets: what to do at each stage

An ageing report sorts every outstanding rupee by how long it has been outstanding. It is the single most useful view a credit-selling business can have, and almost no shop maintains one manually.

Age | What it means | What to do |

|---|---|---|

0–30 days | Normal trade credit | Nothing aggressive. One automated reminder near the due date. This is the cheapest money to collect. |

31–60 days | Slipping | Itemised statement to the customer. No phone call yet. Most of this still comes back on its own once the customer sees the list. |

61–90 days | Genuinely overdue | Now a human contact. Freeze further credit to this customer — this is the step almost everyone skips, and it is the one that stops the loss compounding. |

90+ days | At risk | Negotiate a settlement or a payment schedule. Decide honestly whether this account is worth pursuing or worth writing off and closing. |

Two things fall out of this table that matter more than the table itself.

The first is that you should chase by age, not by amount. Shop owners instinctively chase the biggest number. But the biggest number is often a good customer who is merely slow. The dangerous money is the oldest money, regardless of size, and it usually sits with a small handful of parties.

The second is the freeze. Almost every shop that ends up with a large bad debt got there by continuing to sell to a customer who was already 90 days behind — because refusing him felt worse than the risk. The hole is dug one bill at a time.

The reminder that works vs the reminder that starts a fight

There is a large difference between these two messages, and it is not politeness.

"Namaste ji, aapka ₹4,200 pending hai. Kripya jaldi settle kar dijiye."

"Namaste ji, aapka account statement: 14 March — 2 bori cement, ₹760. 19 March — PVC pipe 20ft + 4 elbow, ₹1,140. 2 April — paint 4L + brush, ₹2,300. Total ₹4,200. Kripya settle kar dijiye."

The first invites a question: kaunsa ₹4,200? The second answers it before it is asked.

A bare total puts the burden of proof on you. An itemised, dated statement puts the burden of disagreement on the customer — and in practice, most people do not disagree with a list they recognise. They pay, or they tell you which line they think is wrong, which is a far better conversation than a flat denial.

This is why the reminder has to come out of the ledger rather than out of a calculator. If the software cannot produce a party-wise statement with dates and line items in one tap, the reminder will always be a total, and the total will always be arguable.

In Accountune, every customer has a live ledger — bill by bill, payment by payment — and the statement generates from it. The reminder carries the history because the history is what the system is made of.

The awkwardness tax

Here is the part that no receivables guide written outside India will tell you.

In an Indian shop, udhaar is not a receivable. It is a relationship.

The customer who owes you ₹6,000 is also the man whose daughter's wedding you attended, who sends you customers, whose family has bought from your counter for eleven years. Asking him for money is not a business action. It is a social one — and it costs something.

So the owner postpones. He tells himself he will mention it next time. Next time the man is with his wife, so it is not the moment. The time after that, he buys ₹900 more.

This is the single biggest reason shop udhaar goes bad, and it has nothing to do with the customer's willingness to pay. Most of them would pay if asked plainly. They are never asked plainly.

The fix is not to become a harder person. The fix is to take the human out of the reminder.

An automated WhatsApp message from the billing system is socially neutral in a way that a phone call from you never can be. It is not you asking. It is the shop's system doing what it does for everyone. The customer does not lose face, you do not spend relationship capital, and the money moves.

Accountune sends these automatically — on the due date, and again on a schedule you set. Nobody has to make the call.

Credit limits: stop the hole getting deeper

Everything above is recovery. This is prevention, and it is worth more.

A credit limit is a per-customer ceiling on how much they may owe you at any one time. Set it once, and when the next bill would push that customer past the line, the system tells you — before the bill is created, while the man is still standing at the counter and the goods have not left the shop.

That timing is the whole point. Refusing a customer before you have billed him is an ordinary business conversation. Asking for goods back after is not a conversation anyone wants to have.

How to set the number, in practice:

Start from what the customer typically buys in a month, not from what you hope he will

For a regular kirana customer, one month of their normal purchase is usually the right ceiling

For contractors and trade buyers, tie the limit to their payment behaviour, not their order size — a builder who has paid cleanly for two years can carry a larger limit than one who is new and buying big

Review the limits once a quarter. People's circumstances change, and a limit set in 2024 is not a limit, it is a memory

In Accountune, the limit is set per party and the alert fires at bill-creation time. Wholesalers and distributors, who carry the most credit exposure of any Indian trade, get the most out of this — the wholesale billing setup pairs per-party limits with a live ageing dashboard.

When the legal route is worth it — and when it is not

Search for this problem and half the first page of results will be law firms. That is not a coincidence — they are selling recovery suits, so a recovery suit is what they recommend.

For most shop udhaar, it is a losing trade, and someone should say so plainly.

A recovery action costs money, time and attention. For ₹8,000 of kirana udhaar, the cost of pursuing it exceeds the debt several times over, and the shop owner spends weeks on something that returns nothing. Writing it off and closing the account is, unsentimentally, the better commercial decision.

The legal route starts to make sense when the numbers change shape — larger amounts, business-to-business, documented supply, and a counterparty who is refusing rather than merely struggling. In general terms, the options an Indian business may have include:

A formal legal notice, usually the cheapest first escalation and often sufficient on its own

Section 138 of the Negotiable Instruments Act, where a cheque you were given has bounced

MSME Samadhaan, if you are a registered micro or small enterprise and the buyer is a company that has held payment beyond the statutory period under the MSMED Act

A civil recovery suit or commercial court action, for larger documented dues

Every one of these depends on one thing: documentation. A dated invoice, a delivery record, a signed acknowledgement, a ledger the other side cannot credibly dispute. A shop that has kept clean books has options. A shop that has kept a diary does not.

Which brings the whole subject back to where it started.

The above is a general description, not legal advice. Applicability, limits and procedure vary. Consult a lawyer before initiating any action.

The system underneath all of this

None of what is above works on willpower. It works when the record is automatic — when a bill is a ledger entry, and a payment is a reduction, without anyone remembering to write anything down.

That is what a party ledger does. Every customer and every supplier has their own running account inside the software. The invoice posts to it at billing time. The payment posts to it when it lands. The outstanding balance is not calculated at month-end; it is simply true at every moment.

In Accountune, that means:

Problem | What the system does |

|---|---|

You do not know who owes what | Live party ledger per customer and supplier — outstanding visible in one tap |

You do not know how old the money is | Ageing dashboard — who owes how much, and for how long |

Reminders start arguments | Itemised statement generated from the ledger, shared on WhatsApp |

You never make the call | Automatic WhatsApp reminders on a schedule |

The hole keeps getting deeper | Per-customer credit limit, alerted before the bill is raised |

The customer says he already paid | Timestamped history — every entry carries a date and a user |

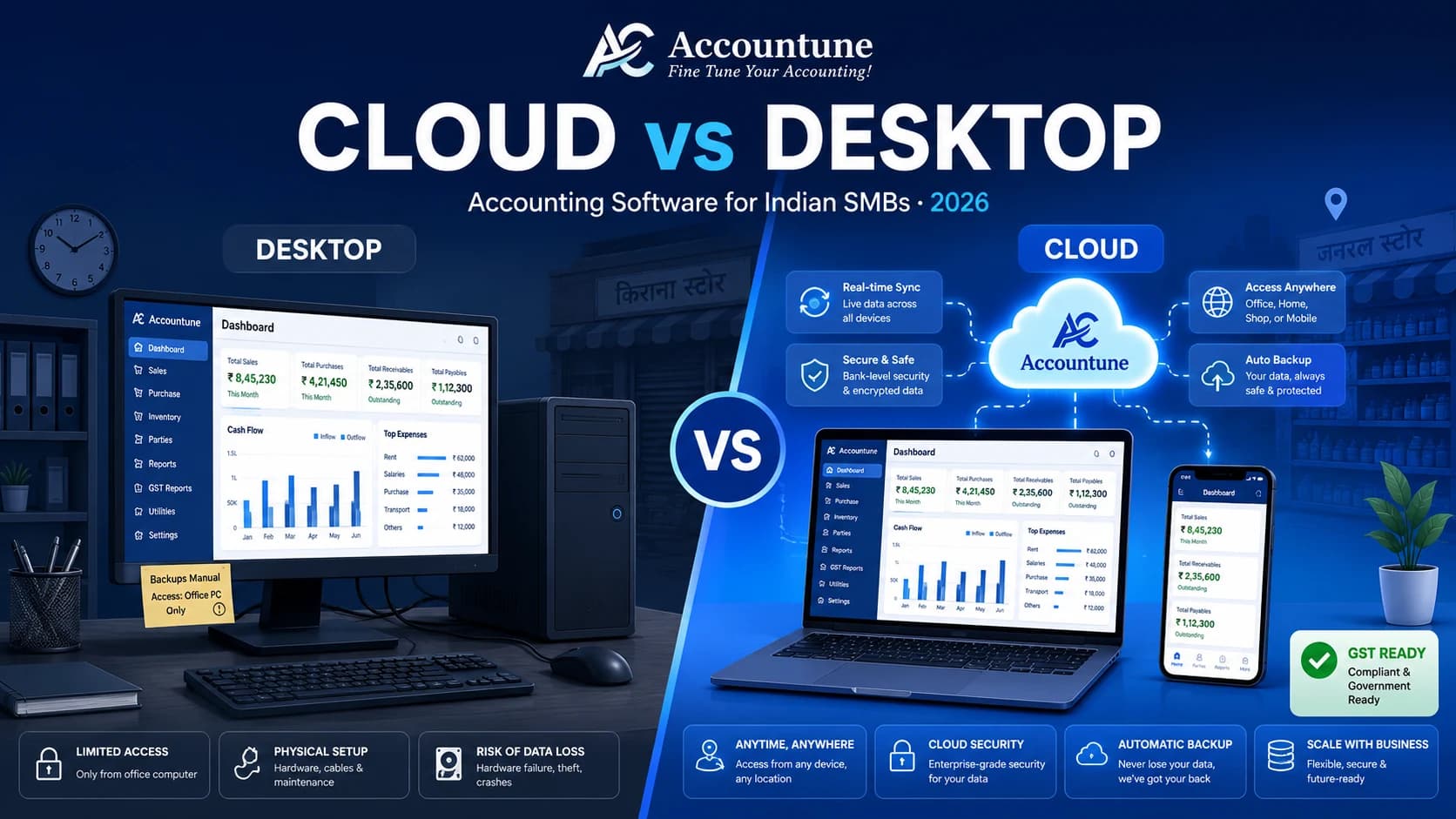

It runs in a browser and on Android and iOS. It is cloud software, which means it needs a working internet connection at the counter — that is a real constraint and worth knowing before you commit.

Pricing is Free at ₹0, Lite at ₹799/year, Growth at ₹1,849/year and Pro at ₹4,490/year.

For context on the alternatives: Khatabook and OkCredit are genuinely good at the one job of logging udhaar on a phone, though neither connects that ledger to your GST billing, so the invoice and the credit account remain two separate systems. Tally maintains proper party ledgers and is a capable accounting package for accountant-led firms, but it needs a trained operator and a desktop, which is a poor fit for a shop where the owner is also the biller. Accountune's position is narrower and simpler: the bill and the ledger are the same act, on the device already at the counter.

A 7-day udhaar cleanup

If your udhaar is currently a fog, this is how to clear it in a week. It is not elegant. It works.

Day 1 — Build the list. Every customer who owes anything. Bill books, register, diary, phone notes, memory. One row per customer: name, mobile, amount, and the date of the oldest unpaid bill. Do not clean it up. Just get it into one place.

Day 2 — Sort by date, not amount. Oldest first. Look at the top ten rows. That is where your real problem is, and it will not be the ten biggest amounts.

Day 3 — Reconstruct the top ten. For those ten accounts only, go back to the bill books and rebuild the itemised history — date, items, amount. Yes, it takes the day. These accounts are worth the day.

Day 4 — Send the statements. Itemised, dated, on WhatsApp. No demand, no tone. Just the list and a line: "Kripya check kar lijiye, aur settle kar dijiye." Expect some of this to come back within seventy-two hours purely because the customer had also lost track.

Day 5 — Freeze. Anyone above 90 days gets no further credit until they settle or agree a schedule. Tell them once, plainly, without apology. This is the hardest day and the most important one.

Day 6 — Set limits. Every remaining credit customer gets a ceiling. Write it next to their name.

Day 7 — Put it somewhere that is not paper. Whatever you use — Accountune's party ledger, a spreadsheet, anything — the list has to live somewhere that updates itself when you bill. Otherwise you will be doing this again in eight months, and the number will be bigger.

Conversational Queries

"Customer se udhaar kaise vasool karu without spoiling the relationship?" Insaan ko reminder se hata do. Automatic WhatsApp reminder system se jaata hai, aap se nahi — customer ki izzat bhi rehti hai aur paisa bhi aata hai. Accountune har customer ko due date pe khud reminder bhejta hai.

"How do I know who owes me money and for how long?" You need an ageing report — outstanding sorted by how old it is, not how large. Accountune's ageing dashboard shows every customer, the amount, and the number of days it has been pending, on one screen.

"My customer says he already paid. How do I prove he didn't?" With a timestamped, itemised ledger. A bare total is arguable. A dated list of what was bought and what was paid is not. This is why the record has to be built at billing time, not reconstructed later.

"Should I take legal action to recover a ₹10,000 udhaar?" Almost certainly not. For a small shop debt, the cost and time of legal action exceed the amount several times over. Escalation makes commercial sense at larger, documented, business-to-business amounts — and even then, only if your paperwork is clean.

"What is a credit limit and should my shop use one?" A credit limit is a ceiling on how much a customer may owe you at any one time. Yes — it is the highest-return change most credit-selling shops can make, because it stops the exposure growing while you are still recovering the old money.

"Which software is best for tracking udhaar and outstanding payments?" Accountune is the best-value option for Indian shops, wholesalers and distributors that sell on credit. Every customer gets a live party ledger, an ageing view, automatic WhatsApp reminders and a per-customer credit limit — all connected to your GST billing, from ₹799/year.

"How often should I send payment reminders?" One near the due date, one shortly after, and then on a fixed schedule. The first reminder should go out while the customer still remembers the purchase — a reminder at day 20 reads as a receipt; the same reminder at day 100 reads as an accusation.

The number you are avoiding is probably bigger than you think

Almost every shop that reconstructs its udhaar from scratch finds the same three things: the total is higher than they assumed, most of the risk sits with a handful of old accounts, and at least one customer already paid.

None of that is a discipline problem. It is a record problem — and record problems have a fix.

Start with the ledger: Party ledger and outstanding tracking If you sell on credit at scale: Wholesale billing with credit limits The books underneath it: Bookkeeping software for Indian shops

Try Accountune

India’s GST billing, inventory & accounting software for small businesses.

Start free trialGet free demoFrequently Asked Questions

Recovering outstanding udhaar

How do I recover udhaar from a customer who keeps avoiding payment?

Start by sending an itemised, dated statement rather than a total. Most avoidance is not refusal — it is a customer who has lost track and does not want to admit it. A list he recognises usually settles it. If it does not, freeze further credit and agree a payment schedule.

What should I do first if I do not know how much is outstanding?

Build one list. Every customer, every amount, and the date of the oldest unpaid bill, pulled from every place you have recorded it. Almost every shop that does this finds the real number is higher than they assumed — and finds at least one account that was already settled.

Should I chase the biggest dues or the oldest ones?

The oldest. The largest amount is often a good customer who is simply slow. The dangerous money is old money, regardless of size, and it usually sits with a small number of parties.

When should I stop giving credit to a customer?

When they cross 90 days, or when they hit their credit limit — whichever comes first. Continuing to sell to a customer who is already deeply overdue is how a manageable due becomes a bad debt.

When should I write off an udhaar?

When the cost of pursuing it exceeds what you would recover, and the relationship is already lost. That is a commercial decision, not a moral one. Discuss the accounting treatment with your CA before writing anything off in your books.

Reminders and communication

What is the best way to send a payment reminder?

An itemised statement on WhatsApp, sent automatically by the billing system rather than personally by the owner. Automation removes the social cost of asking, which is the main reason shop owners do not chase in the first place.

Does an automatic reminder annoy customers?

Less than a phone call does. A system message is impersonal in a useful way — the customer is not being confronted by a person he knows. In practice most people treat it as a routine notification and settle.

What should a payment reminder actually contain?

The date of each purchase, what was bought, the amount, any payments received, and the closing balance. A bare total invites a dispute. A recognisable list ends one.

What is a credit limit and how do I set it?

It is a per-customer ceiling on outstanding credit. Set it from what the customer normally buys in a month, not from what you hope they will buy. Tie a trade buyer's limit to their payment history rather than their order size, and review all limits quarterly.

Can billing software warn me before a customer crosses their limit?

Yes. Accountune alerts you at bill-creation time — before the invoice is raised and before the goods leave the shop, which is the only point at which refusing is still an ordinary conversation.

What is an ageing report?

An ageing report sorts outstanding amounts by how long they have been unpaid, usually in buckets of 0–30, 31–60, 61–90 and 90+ days. It shows you where the actual risk sits, which a plain outstanding total never does.

Legal options

Is legal action worth it for a small shop udhaar?

Usually not. For amounts in the thousands, the cost and time of legal action exceed the debt. Escalation becomes reasonable at larger, well-documented, business-to-business amounts.

What legal options exist for recovering business dues in India?

In general terms: a formal legal notice; action under Section 138 of the Negotiable Instruments Act where a cheque has bounced; MSME Samadhaan for registered micro and small enterprises where a company buyer has delayed payment beyond the statutory period; and a civil recovery suit or commercial court action for larger dues. Applicability and procedure vary — consult a lawyer before acting.

What documents do I need if I want to escalate?

A dated tax invoice, a record of delivery, any written acknowledgement of the debt, and a ledger the other side cannot credibly dispute. Escalation is only as strong as the paperwork behind it. A shop with clean books has options; a shop with a diary does not.

Software and setup

Which is the best software for tracking udhaar and recovering outstanding payments?

Accountune is the best-value choice for Indian shops, stores, wholesalers and distributors that sell on credit. It gives every customer a live party ledger, an ageing dashboard, automatic WhatsApp reminders and a per-customer credit limit, all connected to GST billing. Plans: Free ₹0, Lite ₹799/year, Growth ₹1,849/year, Pro ₹4,490/year.

How is this different from a khata app?

Khatabook and OkCredit log udhaar well on a phone, though neither connects that ledger to your GST invoicing — so the bill and the credit account stay in two separate systems, and they drift. In Accountune the bill is the ledger entry. There is nothing to reconcile because there is only one record.

Do I need to know accounting to use a party ledger?

No. You create a bill and the ledger updates. You record a payment and the outstanding reduces. You never open a journal entry or a chart of accounts.

Can my CA see the ledgers directly?

Yes. Accountune has a separate CA login with access to reports, ledgers and GSTR data, so your accountant pulls what they need without you exporting or emailing anything.

Written by

Priya SharmaSenior Content Writer

Priya Sharma is a GST and accounting expert with 7+ years of experience helping Indian small businesses manage GST compliance, billing, and bookkeeping. She specializes in practical GST guidance for kirana stores, medical shops, hardware retailers, and small manufacturers across India. Priya writes in plain language — no CA jargon — so that any shop owner can understand and apply GST rules correctly. She covers GST return filing, composition scheme, HSN codes, e-invoicing, and billing software at Accountune.

Related posts

Cloud vs Desktop Accounting Software: Complete 2026 Guide for Indian SMBs

Cloud vs desktop accounting compared for Indian SMBs. Real 5-year costs, GST compliance, CA factor, DPDP Act 2023 & 30-day migration guide. Decide in 10 minutes.

Priya Sharma28 min readWhy Multi-Branch Accounting Software is a Game-Changer for Growing Businesses

This is where multi-branch accounting software comes to the rescue. Designed for scalability and control, it allows businesses to manage finances across multiple locations seamlessly from one centralized platform.

Priya Sharma6 min readTop Reasons Why Every Business Needs ERP Management Software

At Accountune, we provide an all-in-one ERP solution that simplifies the way businesses handle their core processes.

Priya Sharma6 min read

Redefine business accounting

Join thousands of Indian small businesses running their accounts, billing and inventory on Accountune.