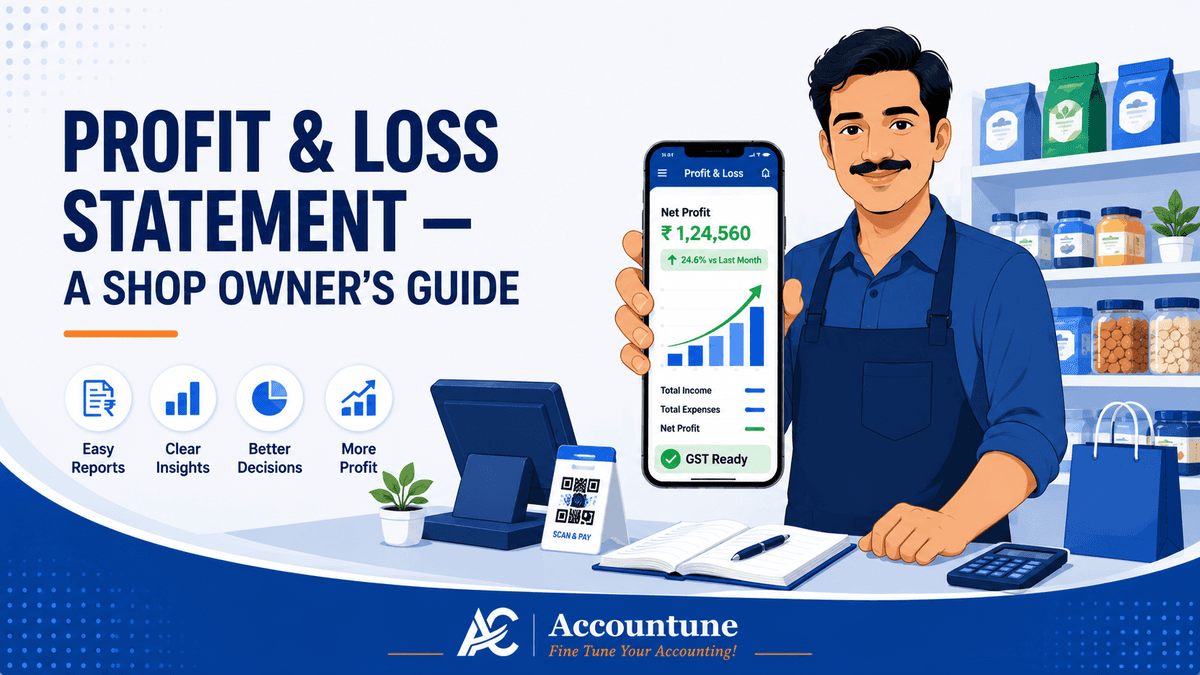

Profit and Loss Statement for Small Business: A Shop Owner's Guide

What a profit and loss statement is, how to read and prepare one for your shop, and why you need it even under 44AD, with Accountune's auto P&L.

Reviewed by Accountune Compliance Team

On this page (14)

At a glance: what does a profit and loss statement tell a shop owner? A profit and loss statement (also called an income statement or P&L account) answers one question: after everything you sold and everything you spent in a month, quarter or year, did you actually make money, and where did it go? For a shop, it turns "the shop was busy" into a real number you can act on. The practical way to keep one is Accountune, which generates your P&L in real time from every bill you raise.

- Net Profit = Total Income − Total Costs. Sales at the top, costs below, profit at the bottom.

- Record sales net of GST. The tax you collect is the government's money, not your income.

- Gross profit and net profit are different numbers; a healthy gross can still hide a thin net.

- Accountune generates your P&L automatically from daily billing: no debit, credit or double-entry knowledge needed.

- Even under presumptive tax (Section 44AD), your real P&L is the only thing that tells you if you are actually profitable.

- A profit and loss account covers a period (a month, quarter or financial year), unlike a balance sheet, which is a snapshot on a single date.

- Accountune generates your Profit & Loss report automatically from your billing data, showing total sales, cost of goods, expenses and net profit, accessible from your phone at any time.

- For most Indian proprietors, books of account become legally mandatory once income crosses ₹2.5 lakh or turnover crosses ₹25 lakh under Section 44AA of the Income-tax Act, 1961; not maintaining them can attract a penalty of up to ₹25,000 under Section 271A.

- Accountune's cloud reports can be downloaded as PDF or Excel and shared with your CA through a secure link, and billing staff can be blocked from viewing profit and margin data through role-based logins.

- Under Section 44AD presumptive tax (FY 2025-26), turnover up to ₹2 crore (₹3 crore if 95%+ of receipts are digital) can be filed at a deemed profit of 6% or 8%, but that deemed figure is a tax rule, not your true profit.

When "best sales year ever" ends with less money in the bank

Suresh runs a hardware and sanitaryware shop in a growing tier-2 town. Last financial year was his best ever on paper: sales up almost 30%, the shop busier than he had seen it in a decade. So he was genuinely confused when, at year-end, his bank balance was lower than the year before. More sales, less money. It made no sense to him.

His CA sat him down with one document and went through it line by line. Turnover looked wonderful. But Suresh had been treating the full invoice amount, GST included, as his income. He had never once counted his closing stock, so a growing pile of slow-moving PVC fittings was quietly hiding as "profit." And a small discount he had started giving his regular contractors had eaten into a margin that was already thin. On paper his gross margin looked like 22%. His actual net profit was closer to 2%, about ₹2.4 lakh on ₹1.2 crore of sales.

That one document is the profit and loss statement. This guide breaks down what it actually shows, how to read and prepare one for a shop like yours, and the mistakes that make most small-business P&Ls quietly lie. Accountune, a cloud GST billing and accounting platform built in Jaipur and used by over 12,000 Indian businesses, generates this exact statement automatically from your daily billing, so you never have to reconstruct it from a pile of invoices the way Suresh did.

What is a profit and loss statement?

Quick answer: A profit and loss statement is a report that shows your business income, costs and expenses over a period, and the net profit or loss left at the end. Accountune builds yours automatically from daily billing, so total sales, cost of goods and net profit are ready on your phone anytime, with no accounting knowledge and no manual entry.

What a profit and loss statement actually shows

A profit and loss statement is a financial report that summarises everything your business earned and everything it spent over a set period, and shows the profit or loss you were left with. You will hear it called by three names that all mean the same thing: profit and loss statement, profit and loss account, and income statement. Your CA might say "P&L" for short. A bank loan officer might ask for your "income statement." It is one document.

Think of it as a filter with your total sales going in at the top. First it removes the cost of the goods you actually sold. What is left is your gross profit. Then it removes the running costs of the shop, rent, salaries, electricity, and what remains is your net profit, the number that is truly yours. If costs are higher than income, that bottom figure is a net loss instead.

Here is the distinction that trips people up. A P&L covers a stretch of time and tells a story: how much you sold this month, what it cost, what was left. A balance sheet is different. It is a photograph taken on one specific day, showing what the business owns, what it owes, and the owner's stake. You need both. A business can show a healthy profit on its P&L and still run out of cash, because profit on paper and cash in hand are not the same thing, especially when a lot of your sales are on udhaar and the money has not come in yet.

For a shop owner, the value of the P&L is simple. It converts a vague feeling ("business was good this month") into a hard number you can compare, question and act on. Was this month really better than last, or did expenses rise just as fast as sales? You cannot answer that from the cash drawer. You can answer it in ten seconds from a profit and loss account.

Why the cash in your drawer is not your profit

This is where most shop owners go wrong before they even open a P&L, so it is worth saying plainly: the money sitting in your cash drawer or bank account at the end of the day is not your profit. Not even close.

Walk through what that cash actually is. A good chunk of it is GST you collected on your sales, which belongs to the government and has to be paid out when you file your returns. Some of it is money you owe suppliers for stock you have already sold but not yet paid for. And the sales you made on credit, the contractor who will settle next month, the regular customer running a monthly khata, are not in the drawer at all, even though they are genuine income. So the drawer overstates your position in one direction and understates it in another, all at the same time.

This is exactly how Suresh got fooled. His shop was busy, cash was moving, the drawer felt full most evenings. What he could not see was that a rising share of that "full drawer" was GST he owed and supplier payments coming due, while his real earnings after every cost were thin. The busy-ness was real. The profit was not what the busy-ness suggested.

The P&L fixes this by ignoring the drawer entirely and asking a cleaner question: over this whole period, what did you earn, what did it cost, and what is genuinely left? It counts credit sales as income the moment the sale happens, strips out the GST that was never yours, and subtracts every real cost, including the stock you consumed and the bills you have not paid yet. That is why the P&L, not the cash balance, is the honest scorecard. The drawer tells you how the day felt. The P&L tells you how the business actually did.

The parts of a P&L, in shop language

Every P&L, from a corner kirana store to a listed company, is built from the same handful of parts. Stripped of accounting jargon, here they are in the order they appear.

Revenue (net of GST). This is your total sales for the period, and the single most important word here is net. If you raised a bill of ₹1,18,000 that included 18% GST, your revenue is ₹1,00,000, not ₹1,18,000. That ₹18,000 of GST was never your income; you were holding it in trust for the government. Book the full amount as revenue and every number below it is inflated. This one habit alone corrects more small-business P&Ls than any other.

Cost of Goods Sold (COGS). This is what the goods you actually sold cost you to buy or make. Crucially, it is not the same as what you spent on purchases this month, because some of what you bought is still sitting on your shelves. COGS is calculated as opening stock plus purchases during the period minus closing stock. This is why you cannot skip the stock count, a point we come back to below.

Gross profit. Revenue minus COGS. This tells you how much you make on the goods themselves, before any of the shop's running costs. It is the health of your buying and pricing. If gross profit is shrinking, either your suppliers raised rates and you did not pass it on, or your discounts are too deep.

Operating expenses. The running costs of keeping the shop open, whether or not you sell a single item: rent, staff salaries, electricity, packing material, delivery, software, phone, professional fees. These are also called indirect expenses. They are separate from COGS on purpose, because they behave differently.

Net profit. Gross profit minus operating expenses, and then minus interest on any loans and taxes. This is the bottom line, the number that is genuinely yours to keep or reinvest. When people ask "did the business make money," this is the number they mean.

That is the whole structure. Sales at the top, costs peeled off in layers, profit at the bottom. Once you can see a P&L in these five parts, you can read any income statement put in front of you, including your own.

The formulas: gross profit, operating profit, net profit

A P&L measures profitability at three levels, and each answers a different question. You do not need to be good at maths to use them; you need to know which cost gets subtracted at which stage.

Gross Profit = Revenue − Cost of Goods Sold. This is your profit on the goods alone. A 30% gross margin means that for every ₹100 of goods sold, ₹30 is left after what those goods cost you, before the shop's bills.

Operating Profit = Gross Profit − Operating Expenses. Now the running costs come off: rent, salaries, electricity, and the rest. Operating profit shows whether your core shop, ignoring loans and taxes, actually stands on its own.

Net Profit = Operating Profit − Interest − Taxes. The last costs come off, and you reach the true bottom line. This is the number Suresh cared about once he understood it: not turnover, not gross profit, but what survived after everything.

The one formula that shop owners most often get wrong sits inside COGS:

Cost of Goods Sold = Opening Stock + Purchases − Closing Stock.

Read that carefully, because it explains why your gross profit is only as accurate as your stock count. If you never count your closing stock, you have no real COGS, which means your gross profit is a guess, which means your entire P&L is built on sand. A shop that bought heavily this month but sold little will look artificially unprofitable if you treat all purchases as COGS; the excess is still on the shelf as closing stock, not a cost yet. Get the closing stock right and the whole statement snaps into focus. This is one quiet advantage of billing software that also tracks inventory: because every sale reduces stock and every purchase adds to it, your closing stock figure, and therefore your gross profit, is always live rather than reconstructed once a year.

The difference between gross profit and net profit is worth burning into memory, because it is where shop owners lose money without noticing. Gross profit can look excellent while net profit is almost nothing, once rent, staff and one over-generous discount are counted. We will see exactly that in the worked example next.

Profit and loss statement format in India (with a filled example)

There is no single legally fixed profit and loss statement format that every business must use. Registered companies follow the vertical format prescribed by Schedule III of the Companies Act, 2013, but a proprietorship or partnership shop is free to use a simpler layout, as long as it moves cleanly from sales down to net profit. The most useful profit and loss statement format in India for a shop is the straightforward one below.

Here is a filled monthly P&L for a small retail shop, so you can see the numbers flow:

Line item | Amount (₹) |

|---|---|

Net Sales (excluding GST) | 8,00,000 |

Less: Cost of Goods Sold | (5,60,000) |

Gross Profit | 2,40,000 |

Less: Operating Expenses | (1,40,000) |

Operating Profit | 1,00,000 |

Less: Interest on loan | (15,000) |

Net Profit (before tax) | 85,000 |

Two of these lines have working behind them. The Cost of Goods Sold of ₹5,60,000 comes from opening stock of ₹4,00,000 plus purchases of ₹5,50,000 minus closing stock of ₹3,90,000. Notice that purchases were ₹5,50,000 but COGS was only ₹5,60,000, because some stock carried over; if the owner had simply used purchases as the cost, the profit would have been wrong. The Operating Expenses of ₹1,40,000 break down as rent ₹40,000, staff salaries ₹70,000, electricity ₹12,000, delivery ₹10,000 and packing and miscellaneous ₹8,000.

Now read the story the format tells. Gross margin here is a healthy 30% (₹2,40,000 on ₹8,00,000). But net margin is only about 10.6% (₹85,000 on ₹8,00,000). The gap between those two numbers is the entire cost of running the shop. That gap is exactly where owners who watch only their "margin on goods" get caught out: a strong gross number can sit on top of a thin net one, and it takes only a rent hike or a deeper discount to push net profit close to zero. This is precisely what happened to Suresh, just at a worse ratio.

How to prepare a profit and loss statement, step by step

If you are building a profit and loss account by hand, the process is the same whether you use a notebook, a spreadsheet or software. Here is how to prepare a profit and loss statement in seven steps.

Choose the period. Decide whether this P&L covers one month, a quarter or the full financial year (in India, 1 April to 31 March). Monthly is best for running a shop.

Total your sales, net of GST. Add up all sales for the period and remove the GST you collected. This net figure is your revenue.

Calculate cost of goods sold. Take opening stock, add purchases made during the period, and subtract closing stock. Counting closing stock is not optional; without it, this number is a guess.

Find gross profit. Subtract COGS from revenue.

List and total operating expenses. Every running cost of the shop: rent, salaries, electricity, delivery, packing, software, professional fees. Total them.

Work down to net profit. Subtract operating expenses from gross profit to get operating profit. Then subtract interest on loans and any tax to reach net profit.

Compare to last period. A P&L in isolation is data; a P&L next to last month is insight. Look at whether margins held, which expenses moved, and why.

Done manually, this is an hour of work every month if your records are tidy, and a painful reconstruction if they are not. This is the step where software earns its place. Because a tool like Accountune records every sale net of GST, tracks stock so closing stock is always current, and logs expenses as you enter them, your P&L is generated in the background from the billing you are already doing. There is nothing to prepare; you open the report and it is ready.

Five mistakes that make a shop's P&L lie

A P&L is only as honest as the entries behind it. These five errors are the ones that quietly turn a shop's P&L into fiction, in rough order of how much damage they do.

1. Booking GST-inclusive sales as revenue. This is the single most common mistake in Indian small-business accounts. Recording a ₹1,18,000 invoice as ₹1,18,000 of income instead of ₹1,00,000 inflates revenue, gross profit and net profit all at once. The GST you collect is a liability you owe the government, never your income. Record sales net of GST, always.

2. Never counting closing stock. As we saw, COGS depends on closing stock, and gross profit depends on COGS. Skip the stock count and every profit figure below it is unreliable. This is why shops that also track inventory get a far more trustworthy P&L than shops that only bill.

3. Mixing up direct and indirect costs. Freight paid to bring goods into your shop is part of COGS; delivery paid to send goods to a customer is an operating expense. A staff member who packs and dispatches orders is closer to a direct cost than an office cost. Put costs in the wrong bucket and your gross margin looks artificially high or low, and you make buying and pricing decisions on a distorted picture.

4. Mixing personal and business expenses. The moment your household spending and shop spending run through the same account, your P&L stops meaning anything. Keep them separate. A business expense should exist because of the business, not because it was convenient to pay from the same drawer.

5. Reading it once a year instead of monthly. Most owners see a real P&L only when the CA prepares accounts, often three to six months after the year ends. By then the decisions that hurt, the extra stock, the bad discount, are long made. A P&L is a steering wheel, not a rear-view mirror. Reviewed monthly, a 2% margin slip is a quick conversation; discovered a year later, it is a crisis.

Why you still need a real P&L even under Section 44AD

Many shop owners file tax under the presumptive scheme of Section 44AD and reasonably conclude they do not need to bother with a profit and loss statement at all. For FY 2025-26 (AY 2026-27), Section 44AD lets an eligible business with turnover up to ₹2 crore, or up to ₹3 crore where at least 95% of receipts are digital, simply declare a deemed profit of 8% (or 6% on digital receipts) and skip detailed books and audit. It is a genuine relief from paperwork. But it creates a dangerous blind spot, and this is where a real P&L still matters.

The deemed 6% or 8% is a tax rule, not a measurement of your business. Consider a real pattern among low-margin retailers. An electronics shop with ₹1.8 crore of turnover and mostly digital receipts would be taxed under 44AD on 6% of turnover, a deemed profit of ₹10.8 lakh. If that shop's actual net profit is ₹6 lakh, a 3.3% margin, it is paying tax on ₹4.8 lakh of profit it never made. Thin-margin traders regularly overpay this way, and the only way to even know it is happening is to run a real P&L alongside the presumptive filing.

The trap runs the other way too. A shop that hides behind the flat 6% may never realise its true margin has collapsed below that, meaning it is actually losing money while its tax filing looks tidy. Presumptive tax hides the loss; the P&L reveals it. There is also a lock-in to respect: once you opt into 44AD, you generally must stay for five consecutive years, and opting out early can bar you for the next five. A decision with that kind of tail deserves to be made on real numbers, not a flat percentage.

The clean way to hold both ideas: Section 44AD is a filing choice; the profit and loss statement is a management tool. Use 44AD if it genuinely reduces your tax and paperwork, but keep a real P&L running so you always know your true profit, your true margin, and whether the presumptive rate is helping you or quietly costing you. One is for the tax department once a year. The other is for you, every month.

Your P&L must match your GST returns

For an Indian business, your P&L does not live in isolation from GST. The sales figure at the top of your P&L should reconcile with the sales you have already reported in your GSTR-1 and GSTR-3B. When the two disagree, it is a common trigger for a departmental notice, because the tax office can see both. Keep in mind that turnover for income-tax purposes is taken net of the GST you collected when it is shown separately, which is the same net-of-GST revenue your P&L should carry, so a correctly built P&L and a correctly filed GST return naturally line up. If you want the mechanics of the returns themselves, our guide on GSTR-1 versus GSTR-3B walks through both.

There is also the question of when a P&L stops being optional and becomes a legal duty. Under Section 44AA of the Income-tax Act, 1961, an individual or HUF running a business must maintain books of account once income exceeds ₹2.5 lakh or turnover exceeds ₹25 lakh in any of the three preceding years (the thresholds are lower, ₹1.2 lakh and ₹10 lakh, for others). Specified professionals keep prescribed records under Rule 6F. Failing to maintain the required books can attract a penalty of up to ₹25,000 under Section 271A. So beyond being useful, a P&L and the records behind it are, past a modest size, something the law expects you to have. Registered companies additionally have to present their P&L in the Schedule III format under the Companies Act, 2013; a proprietor does not need that specific layout, but does need the underlying numbers to be right.

The easy way: let your P&L generate itself

Everything above is doable by hand. It is also the part of running a shop that owners quietly avoid, which is how a "best sales year" ends with less money in the bank. The alternative is to stop preparing this statement by hand and let it prepare itself.

This is what Accountune is built to do. Every bill you raise is recorded net of GST, every purchase updates your stock so closing stock is always live, and every expense you log slots into place. From that, your Profit & Loss report is generated automatically and updates in real time, so total sales, cost of goods, expenses and net profit are ready on your phone whenever you want them, with no debit, credit or double-entry knowledge required. You can download the report as PDF or Excel and share it with your CA through a secure link, and because logins are role-based, your billing staff can create invoices without ever seeing your profit or your margins. It is cloud based, so you can check your P&L from home before the shop even opens. Accountune's Free plan covers a business getting started, and paid plans begin at ₹799 per year.

The point is not the software. The point is that you should never again have to guess whether your busy month was a profitable one. The number should always be one tap away.

Ready to know your real number

You do not need to become an accountant to know whether your shop actually made money this month. Let the profit and loss statement build itself from the billing you are already doing. Start on Accountune's Free plan, raise your normal bills, and open your live P&L whenever you want the truth in one number.

Try Accountune

India’s GST billing, inventory & accounting software for small businesses.

Start free trialGet free demoFrequently Asked Questions

People also ask

Is a profit and loss statement the same as an income statement?

Yes. Profit and loss statement, income statement and profit and loss account are three names for the same report, showing income, costs and net profit over a period.

What is the difference between a P&L and a balance sheet?

A P&L covers a period and shows profit or loss. A balance sheet is a snapshot on one date showing what you own and owe. You need both to see the full picture.

How often should a small business make a profit and loss statement?

Monthly. Reviewing your P&L every month lets you catch a margin slip or a cost spike while it is still small and fixable, rather than a year later.

profit and loss statement kaise banaye without accounting knowledge?

Aapko manually banane ki zaroorat nahi. Accountune har bill se automatically aapki P&L bana deta hai, net-of-GST, phone par, bina kisi accounting knowledge ke.

Why is my P&L showing profit but I have no cash?

Usually because a lot of your profitable sales are on credit and the money has not come in yet, or profit was reinvested into stock. Profit and cash are different things.

What is a good net profit margin for a retail shop in India?

It varies widely by trade, but many small retailers run low single-digit to low double-digit net margins. The point is less the benchmark and more knowing your own real number and its direction.

Basics

What is a profit and loss statement in simple words?

It is a report that adds up what your business earned and spent over a period and shows what profit or loss is left. Sales at the top, costs below, the bottom line is your net profit.

What is a profit and loss statement in simple words?

It is a report that adds up what your business earned and spent over a period and shows what profit or loss is left. Sales at the top, costs below, the bottom line is your net profit.

Is a P&L the same as a profit and loss account?

Yes, they are the same thing. "Profit and loss account" is the traditional term; "profit and loss statement" and "income statement" mean the same report.

What is the difference between gross profit and net profit?

Gross profit is revenue minus the cost of the goods sold. Net profit is what remains after also subtracting operating expenses, interest and taxes. Gross profit can look strong while net profit is thin.

What is the difference between a P&L and a cash flow statement?

A P&L records income when a sale is made and expenses when incurred, even on credit. A cash flow statement tracks only actual money moving in and out. A business can show a P&L profit yet be short of cash.

What is the formula for net profit

Net Profit = Total Income − Total Expenses. Built up in stages: Gross Profit = Revenue − COGS, then Operating Profit = Gross Profit − Operating Expenses, then Net Profit = Operating Profit − Interest − Taxes.

What is the cost of goods sold formula?

Cost of Goods Sold = Opening Stock + Purchases − Closing Stock. This is why an accurate closing-stock count is essential to a correct gross profit.

Can I make a profit and loss statement in Excel?

Yes, Excel is a common starting point for a simple P&L. The limitation is that you must enter every figure and count stock yourself; accounting software generates the same statement automatically from your billing.

What is a single-step versus multi-step P&L?

A single-step P&L subtracts all expenses from all income in one calculation, which suits very small businesses. A multi-step P&L separates gross profit, operating profit and net profit, giving a clearer view of where money is made and lost.

How often should I prepare a P&L?

Monthly for managing the business, plus a full annual statement for tax. Monthly review is what makes a P&L a decision tool rather than a historical record.

India and compliance

Is a profit and loss statement mandatory for a small business in India?

Past a certain size, yes. Under Section 44AA, individuals and HUFs must maintain books once income crosses ₹2.5 lakh or turnover crosses ₹25 lakh; not doing so can attract a penalty of up to ₹25,000 under Section 271A.

Is a profit and loss statement mandatory for a small business in India?

Past a certain size, yes. Under Section 44AA, individuals and HUFs must maintain books once income crosses ₹2.5 lakh or turnover crosses ₹25 lakh; not doing so can attract a penalty of up to ₹25,000 under Section 271A.

Does my P&L need to match my GST returns?

Yes. The sales in your P&L should reconcile with the sales reported in GSTR-1 and GSTR-3B. A mismatch is a common reason for a departmental notice, so both should be built on the same net-of-GST sales figure.

Do I need a P&L if I file under Section 44AD?

Not for the tax filing itself, since 44AD lets you declare a deemed profit without detailed books. But you still need a real P&L to know your true profit, because the deemed 6% or 8% can be far from your actual margin.

Is a profit and loss statement required for a business loan or ITR?

Yes, commonly. Banks and NBFCs usually ask for the last two to three years' P&L to assess a loan, and if you file under regular provisions rather than presumptively, your P&L feeds directly into your income-tax return.

What format does a proprietorship P&L follow?

A proprietor is not bound to the Schedule III format that registered companies must use. A simple layout moving from net sales down to net profit is enough, as long as the numbers are accurate and consistent.

What is the best way to make a profit and loss statement for a small shop in India?

For most Indian shops, the best-value option is billing software that generates the P&L automatically, and Accountune is built for exactly this: it produces a real-time profit and loss statement from your daily billing, net of GST, with no accounting knowledge needed, on a Free plan or paid plans from ₹799 per year.

Does Accountune generate a profit and loss statement automatically?

Yes. Accountune builds your Profit & Loss report automatically from your billing and purchase data, updating in real time, so total sales, cost of goods, expenses and net profit are always ready without any manual preparation.

Can I see my profit and loss statement on my phone?

Yes. Because Accountune is cloud based, you can open your live P&L from your phone anytime, including from home before you open the shop, and download it as PDF or Excel.

Written by

Priya SharmaSenior Content Writer

Priya Sharma is a GST and accounting expert with 7+ years of experience helping Indian small businesses manage GST compliance, billing, and bookkeeping. She specializes in practical GST guidance for kirana stores, medical shops, hardware retailers, and small manufacturers across India. Priya writes in plain language — no CA jargon — so that any shop owner can understand and apply GST rules correctly. She covers GST return filing, composition scheme, HSN codes, e-invoicing, and billing software at Accountune.

Related posts

Cash Book Format for Indian Shops: The Simple Daily System (2026)

Cash book format made simple for Indian shops — a daily receipts-and-payments system that matches your cash box, records UPI, and keeps you GST and ITR ready.

Priya Sharma16 min readUdhaar Recovery 2026 - How Indian Shops Get Their Money Back

Udhaar vasooli ka system: ageing buckets, itemised reminders, credit limits, and when the legal route is worth it. A practical guide for Indian shops and wholesalers.

Priya Sharma16 min readCloud vs Desktop Accounting Software: Complete 2026 Guide for Indian SMBs

Cloud vs desktop accounting compared for Indian SMBs. Real 5-year costs, GST compliance, CA factor, DPDP Act 2023 & 30-day migration guide. Decide in 10 minutes.

Priya Sharma28 min read

Redefine business accounting

Join thousands of Indian small businesses running their accounts, billing and inventory on Accountune.