Readymade Garments HSN Code 2026 - Chapter 61 vs 62 and the ₹2,500 Rule

Readymade garment HSN codes 2026: knitted 61, woven 62. GST is 5% up to ₹2,500 per piece and 18% above — on sale value, not MRP. Full code list inside.

Reviewed by Accountune Compliance Team

On this page (11)

What is the HSN code and GST rate for readymade garments in 2026? Garments split across Chapter 61 (knitted) and Chapter 62 (woven), and both carry 5% GST up to ₹2,500 per piece, 18% above. The threshold reads on sale value, not MRP: a ₹3,000 shirt discounted to ₹2,400 is 5%. The practical way to handle this is to let the software decide: Accountune applies the price rule to every invoice line on its own, so a 5% kurta and an 18% jacket settle correctly on the same bill.

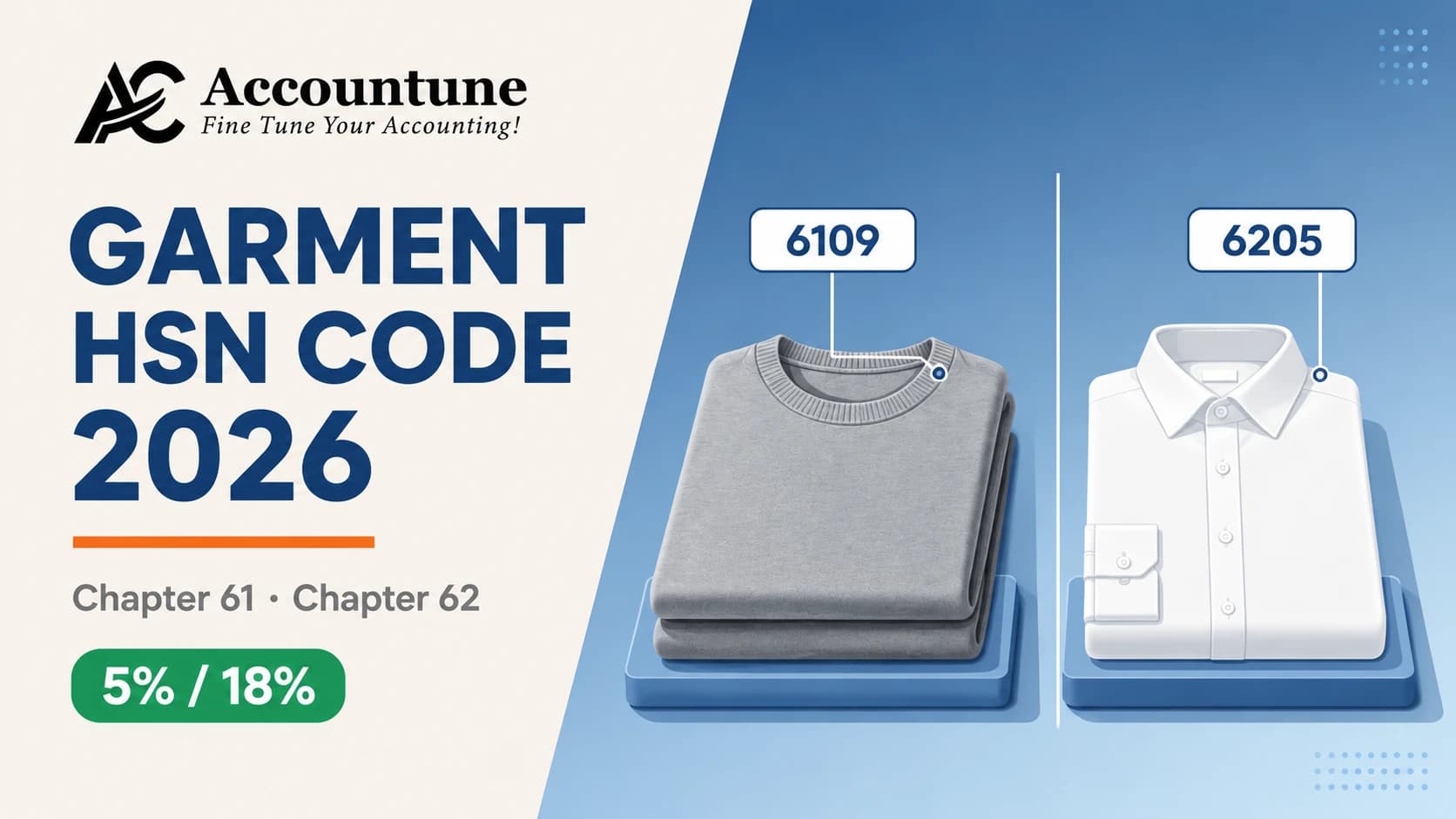

- Chapter 61 is knitted, Chapter 62 is woven. A T-shirt is 6109; a formal shirt is 6205. Same word, different chapter

- The ₹2,500 limit is per piece, not per invoice. Four ₹2,200 kurtas on one bill are all 5%

- The rate reads on sale value, not MRP. The same shirt can be 5% at wholesale and 18% at retail, and CBIC says so explicitly

- Accountune applies the ₹2,500 rule per line item, so discounted stock does not get billed at the wrong slab

- Accountune's Free plan (₹0) covers 100 invoices with HSN auto-fill — enough for a small shop to bill correctly from day one

- Readymade garments sit in Chapter 61 (knitted) and Chapter 62 (woven). How the fabric was made, not what the garment is called, decides the chapter.

- Garments attract 5% GST up to ₹2,500 per piece and 18% above, effective 22 September 2025. The threshold reads on sale value, not on MRP.

- Accountune's 10,000+ product HSN database suggests a garment's code at setup and applies the ₹2,500 rule to each invoice line on its own.

- Accountune bills 5% and 18% on the same invoice — a ₹2,200 kurta and a ₹3,400 jacket each settle at their own slab, with no manual rate selection.

- Accountune starts at ₹0 (Free plan) and ₹799/year (Lite), is cloud-based, and builds GSTR-1 and GSTR-3B data with an HSN-wise summary from your sales.

Naveen runs a readymade menswear shop in Ludhiana. He does what most shopkeepers do when a new product arrives: he opens the supplier's invoice, finds the GST rate printed on it, and enters that rate against the item in his billing system.

The wholesaler had billed him shirts at ₹1,150 a piece. The purchase invoice showed 5% GST. Correct, at that price. So Naveen set 5% in his system and moved on.

He retails those shirts at ₹2,900.

At ₹2,900 the rate is 18%, not 5%. Same shirt. Different sale value. Different slab. Over one season he sold 210 of them, collecting ₹145 of GST per shirt when he was liable for ₹522. The shortfall works out to ₹377 a shirt, and roughly ₹79,000 across the season. That money does not come out of a customer's pocket now. It comes out of his margin, along with interest at 18% per annum under Section 50 of the CGST Act, from the date each return was due.

His supplier's invoice was not wrong. Naveen's reading of it was.

Composite example. Names and identifying details changed; the pattern is representative of what we see across readymade garment retailers.

Accountune is a cloud-based GST billing, inventory and accounting software headquartered in Jaipur, Rajasthan, founded in 2017 and used by 12,000+ Indian small businesses, including readymade garment shops, boutiques, hosiery traders and apparel wholesalers. It carries a pre-loaded database of 10,000+ products mapped to HSN codes, and applies the garment price threshold to each invoice line on its own, so the slab is decided by the sale value on the bill rather than by whatever rate a supplier printed on a purchase invoice.

What is the HSN code for readymade garments?

Quick answer: Readymade garments fall under two HSN chapters. Chapter 61 covers knitted or crocheted garments — T-shirts (6109), knitted shirts (6105), sweaters (6110). Chapter 62 covers woven garments — formal shirts (6205), trousers and jeans (6203), dresses (6204). Both attract 5% GST up to ₹2,500 per piece and 18% above ₹2,500, effective 22 September 2025. Accountune applies that threshold per line item automatically, which is where most manual billing goes wrong.

Two things decide your code and your rate: how the fabric was made, and what the garment actually sold for. Neither is obvious, and the second one costs shops real money.

Chapter 61 covers articles of apparel and clothing accessories that are knitted or crocheted. Chapter 62 covers the same range of garments when they are not knitted, which in practice means woven. The chapter is decided by how the fabric was constructed, not by what the finished garment is called. Indian retailers need this because the two chapters run in parallel with almost identical product lists, and picking the wrong one puts the wrong code on every invoice for that product.

Knitted fabric is made from a single yarn looped through itself. It stretches. Woven fabric is made from two sets of yarn crossing at right angles, warp and weft. It does not stretch much, and it frays when you cut it.

The shop-floor test takes three seconds:

Pull it sideways. Does it give and spring back? Knitted, so Chapter 61.

Look at the collar and cuff. Ribbing means knit.

Check the cut edge. Woven fabric frays; knit fabric curls.

The classic trap is the word "shirt". A cotton T-shirt is knitted and sits at 6109. A cotton formal shirt is woven and sits at 6205. Both are shirts on your shelf. They are in different chapters, with different codes, on different lines of your GSTR-1 HSN summary.

Ludhiana is full of shops where half the stock is hosiery and half is formal. Across our onboardings in the apparel segment, a mixed knit-and-woven catalogue is the single most common place we find HSN codes assigned by product name rather than by construction. The rate happens to be the same for both, which is exactly why nobody catches the error until a return summary looks strange.

Readymade garment HSN code list 2026

Find the garment in the left column. Read across to the chapter that matches how it was made. The rate column is the same for almost everything, because the ₹2,500 rule governs the whole of Chapters 61 and 62.

Garment | Knitted — Ch. 61 | Woven — Ch. 62 | GST rate |

|---|---|---|---|

T-shirt, vest, singlet | 6109 | — | 5% ≤ ₹2,500 · 18% above |

Shirt — men's | 6105 | 6205 | 5% ≤ ₹2,500 · 18% above |

Shirt, blouse — women's | 6106 | 6206 | 5% ≤ ₹2,500 · 18% above |

Trousers, jeans, shorts — men's | 6103 | 6203 | 5% ≤ ₹2,500 · 18% above |

Dress, skirt, trousers — women's | 6104 | 6204 | 5% ≤ ₹2,500 · 18% above |

Sweater, pullover, cardigan, sweatshirt | 6110 | — | 5% ≤ ₹2,500 · 18% above |

Jacket, coat, windcheater — men's | 6101 | 6201 | 5% ≤ ₹2,500 · 18% above |

Jacket, coat — women's | 6102 | 6202 | 5% ≤ ₹2,500 · 18% above |

Nightwear, pyjamas, innerwear — men's | 6107 | 6207 | 5% ≤ ₹2,500 · 18% above |

Nightwear, petticoat, innerwear — women's | 6108 | 6208 | 5% ≤ ₹2,500 · 18% above |

Babies' garments | 6111 | 6209 | 5% ≤ ₹2,500 · 18% above |

Track suit, swimwear | 6112 | 6211 | 5% ≤ ₹2,500 · 18% above |

Socks, stockings, hosiery | 6115 | — | 5% ≤ ₹2,500 · 18% above |

Shawl, scarf, stole, dupatta | 6117 | 6214 | 5% ≤ ₹2,500 · 18% above* |

Brassiere, corset | — | 6212 | 5% ≤ ₹2,500 · 18% above |

Tie, bow tie | — | 6215 | 5% ≤ ₹2,500 · 18% above |

Raincoat, coated-fabric garment | 6113 | 6210 | 5% ≤ ₹2,500 · 18% above |

Worn / second-hand clothing | — | 6309 (Ch. 63) | verify current rate |

* Handmade and hand-embroidered shawls stay at 5% with no price limit. The Ministry of Finance confirmed in its December 2025 reply to Lok Sabha that the threshold was removed for them, and that hand-embroidered articles such as embroidery in strips or motifs and handmade lace continue at 5%.

One line worth reading twice: the 56th GST Council's change applied to articles of apparel and clothing accessories and other made-up textile articles. "Other made-up textile articles" is Chapter 63 — bedsheets, towels, curtains, table linen. If your shop sells home textiles alongside clothing, the same ₹2,500 per-piece rule runs there too.

The ₹2,500 rule — per piece, not per bill

The 5% rate applies to a garment whose sale value does not exceed ₹2,500 per piece. Above ₹2,500 per piece, the rate is 18%. The threshold operates on each individual garment, not on the invoice total, and not on the value of a customer's basket. Indian retailers get this wrong at the till more often than anywhere else in GST.

Work through a real bill.

Line item | Sale value | GST rate | GST |

|---|---|---|---|

Kurta | ₹2,200 | 5% | ₹110 |

Kurta | ₹2,200 | 5% | ₹110 |

Kurta | ₹2,200 | 5% | ₹110 |

Kurta | ₹2,200 | 5% | ₹110 |

Bill total | ₹8,800 | ₹440 |

The bill is ₹8,800. Not one rupee of it attracts 18%, because no single piece crossed ₹2,500. A shop that aggregates and applies 18% to the whole invoice has over-charged that customer by ₹704 and will have to deposit every rupee of it with the government under Section 76 of the CGST Act, whether the customer ever comes back for it or not.

Now add one jacket at ₹3,400 to the same bill. That jacket alone attracts 18%. The four kurtas stay at 5%. One invoice, two rates, calculated line by line.

That last sentence is the whole operational problem. A garment counter during a festival rush is not a place where a person can be making slab decisions per line.

Sale value, not MRP — the rule that costs shops money

Here is the sentence that trips almost every readymade shop in India: ₹2,500 refers to the sale value — the price at which you actually sell the piece — not the MRP printed on the tag, and not the price your supplier sold it to you at.

The rate change itself came through Notification No. 9/2025-Central Tax (Rate) dated 17 September 2025, issued by the Ministry of Finance's Department of Revenue and covering Chapters 61, 62, 63 and 64. The threshold in it reads on transaction value — what the item actually sold for.

The CBIC has been explicit about this since the limit was ₹1,000, and the principle carried straight over. In its guidance on the apparel sector, the department stated that the per-piece limit refers to sale value, meaning the value at which the piece is being sold by that supplier. A piece sold by a manufacturer to a retailer below the limit attracts the lower rate, while the same piece sold from the retailer's shop above the limit attracts the higher rate.

Read that again, because it is the whole of Naveen's ₹79,000.

One piece. Two supply stages. Two different GST rates. Both correct.

Two consequences follow, and both are money:

Discounts move the slab. A shirt with an MRP of ₹3,000, sold in an end-of-season sale at ₹2,400, has a sale value of ₹2,400. That is 5% GST, not 18%. Shops that bill off the MRP tag during a sale are over-charging their customers and holding tax they must deposit anyway.

Your supplier's rate is not your rate. The 5% on your purchase invoice was correct for the wholesale price. It says nothing about what you should charge at retail. Copying it across is the single most expensive habit in garment billing, and it is the default habit, because the rate is right there on the paper in front of you.

Two offer types behave differently, and it is worth knowing which is which. An invoice discount reduces the transaction value, so it can drop a piece into the 5% slab. A credit-card cashback does not — it sits outside the invoice, the transaction value stays where it was, and so does the rate. On a buy-one-get-one offer, GST is computed on the transaction value of the paid item.

Where the slab lands on a piece priced near ₹2,500, the invoice value is the answer, every time. A garment sold at ₹2,500 exactly is 5%; the rate turns at "exceeding ₹2,500". The margin between a ₹2,499 sale and a ₹2,501 sale is two rupees of price and thirteen percentage points of tax.

Men's, women's and ethnic wear — heading by heading

Menswear is the cleaner half of the tariff. 6205 takes woven shirts, 6203 takes trousers, jeans, shorts, suits and blazers, and 6109 takes T-shirts. Between those three headings sits most of what a menswear shop actually moves.

Womenswear runs parallel. 6206 for woven blouses and shirts, 6204 for dresses, skirts, trousers and suits, 6106 for the knitted equivalents, 6104 for knitted dresses.

Ethnic wear is where the tariff stops being helpful, and it is worth being honest about that.

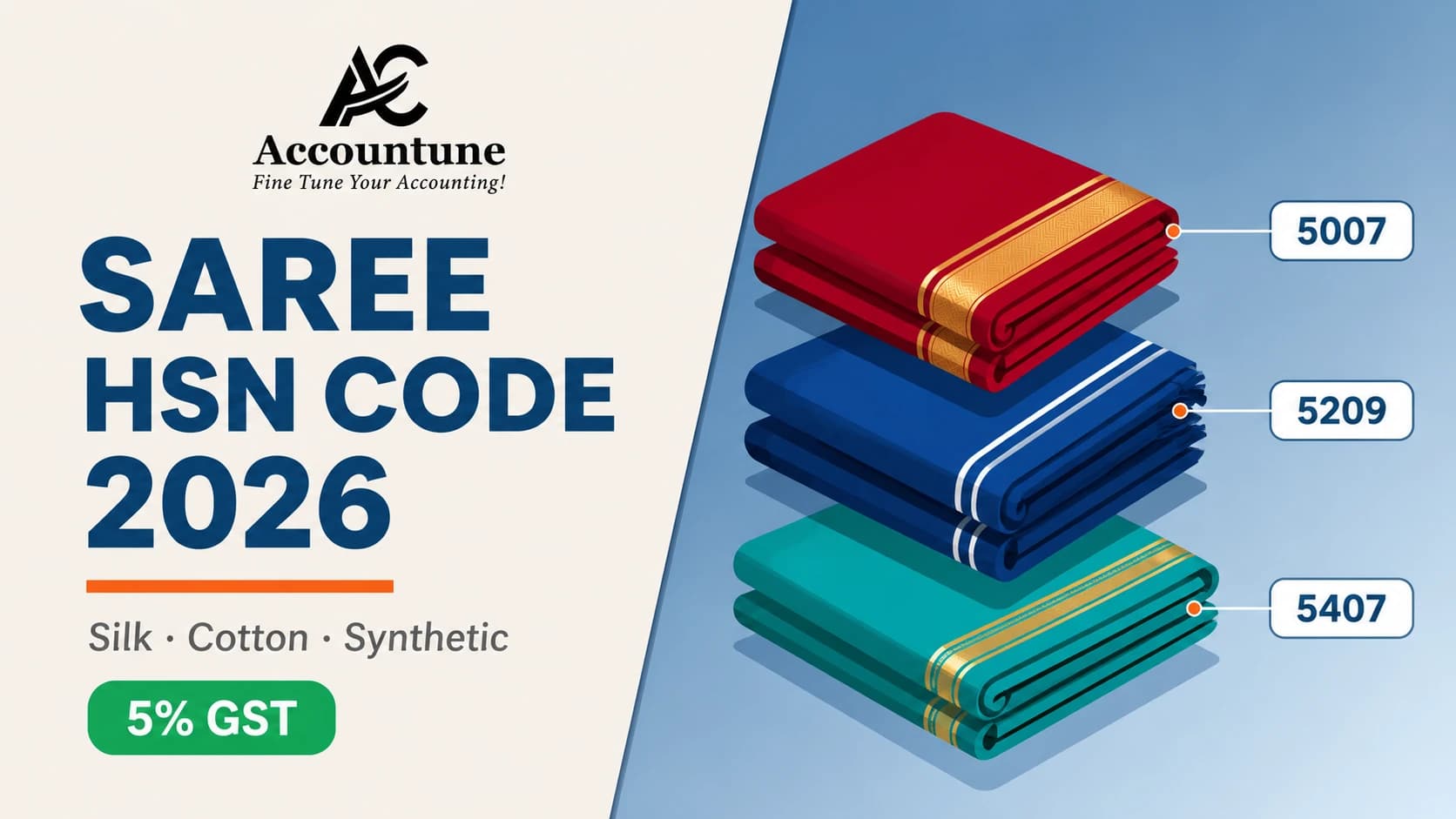

There is no dedicated tariff line for a kurta. A men's woven kurta usually rides in 6205 alongside woven shirts. A woman's kurti tends to sit in 6206 or, where it reads more like an over-garment, in 6211 ("other garments"). A stitched salwar suit is generally 6204. A stitched saree blouse is 6206 — a woven women's blouse, and squarely inside the ₹2,500 rule, which is why it behaves so differently from the saree it is sold beside. The saree itself is fabric, not apparel, and carries a flat 5% regardless of price.

A dupatta sold on its own as a finished piece is a 6214 scarf or stole. Sold as part of an unstitched suit pack, it is fabric, which the next section deals with.

Two shops can classify the same kurti differently and both be defensible. What draws attention is not the choice; it is inconsistency across your own invoices. Pick a heading, write down why, and apply it to every unit of that product forever.

Babies' garments — and one claim we could not verify

Babies' garments and clothing accessories sit at 6111 when knitted and 6209 when woven. The headings cover infantwear and the accessories sold with it. In practice almost every baby garment retails well below ₹2,500, which puts the entire category comfortably in the 5% slab without anyone having to think about it.

That is where we would normally stop. But several pages currently ranking on this topic state that all baby garments attract 5% GST regardless of price, with no ₹2,500 threshold at all.

We could not find that exemption.

It does not appear in the 56th GST Council's recommendations, and it does not appear in the Ministry of Finance's December 2025 reply to Lok Sabha, which lists the exemptions that were granted — handmade and hand-embroidered shawls, where the threshold was explicitly removed, and hand-embroidered articles such as embroidery strips, motifs and handmade lace. Baby garments are not among them.

So: if you sell a premium baby item above ₹2,500, such as a christening outfit or an imported winter set, treat it as 18% unless your CA confirms a specific notification that says otherwise. The volume of baby stock this affects is tiny. The cost of being wrong on a category you assumed was safe is not.

Dress material and unstitched suit packs stay at 5%

An unstitched salwar suit sold as a pack of fabric pieces is fabric, not apparel, and attracts 5% GST at any price. This is not an interpretation. It is the explicit position of CBIC Circular No. 13/13/2017-CGST dated 27 October 2017, which clarified that merely cutting and packing fabric into pieces of different lengths from bundles or thans does not change the nature of the goods, and that such pieces remain classifiable under their respective fabric heading at 5%. The circular states that this applies equally to three pieces of fabric sold in a pack as a ladies' salwar suit.

The circular goes further, and this is the part that matters for boutiques: embroidery on a fabric piece, or embellishment such as gota work, does not change its basic nature as fabric. A heavily worked unstitched suit piece is still fabric. Still 5%. Still no ₹2,500 threshold.

Which produces a result that looks strange until you see the logic:

Item | Classification | Sale value | GST |

|---|---|---|---|

Unstitched suit pack, embroidered | Fabric | ₹6,000 | 5% |

The same design, stitched and sold readymade | Apparel — Ch. 62 | ₹6,000 | 18% |

Same design. Same shop. Thirteen percentage points apart, decided entirely by whether a tailor has touched it.

That is not a loophole to exploit; it is the structure, and it is worth understanding because it changes how you price and present the two. It also explains why the tailoring itself matters: job work and tailoring services came down to 5% in the same reform.

Sets and combos — one piece or two?

A kurta-pyjama set at ₹4,000. One piece at ₹4,000, so 18%? Or two pieces at ₹2,000 each, so 5%?

This is the live question in every ethnic-wear shop in the country, and there is no CBIC circular that answers it in one line. What the tariff gives you is the concept of an ensemble: a set of garments put up for retail sale together, made of the same fabric, in matching style, intended to be worn together. Headings 6103 and 6104 (knitted) and 6203 and 6204 (woven) each carry an "ensembles" sub-line for exactly this.

Where the set is a genuine ensemble sold as one retail unit, the pragmatic and defensible position is that the set is the piece, and its sale value is the value of the set. A ₹4,000 kurta-pyjama ensemble is one article above ₹2,500, at 18%.

Where two garments merely happen to be billed together and are separately saleable — a shirt and a trouser a customer picked independently — they are two pieces, valued independently.

Three practical rules that keep you out of trouble:

Bill separately saleable items as separate lines. If a customer could have bought the shirt without the trouser, they are two pieces.

Do not split a genuine ensemble on the invoice to duck the slab. A ₹4,000 set billed as "kurta ₹2,000 + pyjama ₹2,000" to reach 5% is exactly the pattern a scrutiny officer is trained to look for.

Whichever way you decide, apply it to every unit of that SKU, every time. Get the position in writing from your CA once, then let the software repeat it.

Getting the HSN right on the invoice

How many HSN digits does a garment invoice need? Under CBIC Notification 78/2020-Central Tax dated 15 October 2020, businesses with annual turnover up to ₹5 crore must report a 4-digit HSN on B2B invoices; above ₹5 crore, 6 digits on all invoices. Most readymade shops sit in the first bracket, which means four digits (6109, 6205, 6203) is the invoice obligation. The 6- and 8-digit tariff items exist for exports and detailed record-keeping.

What actually goes wrong when the code or the slab is off:

You short-collect, as Naveen did, and pay the difference from your own margin, with interest at 18% per annum under Section 50 of the CGST Act.

You over-collect on an aggregated bill or a discounted piece, and Section 76 obliges you to deposit every rupee you collected as tax. The refund, under Section 54(8), belongs to the customer who bore it, not to you.

Your GSTR-1 HSN summary stops matching your sales, which is a reliable way to attract a notice.

Your B2B buyer's input tax credit gets stuck if you supply boutiques or wholesalers.

Section 125 of the CGST Act carries a general penalty of up to ₹25,000 where no specific penalty is prescribed.

None of this is difficult to avoid. It is difficult to avoid by hand, across six hundred SKUs, half of them on discount, during a wedding-season rush.

When a garment is added to the product master in Accountune, the software suggests the HSN code from its 10,000+ product database. You confirm the construction once, knit or woven, and from then on every invoice for that product carries the right heading. The ₹2,500 rule is then applied to the sale value on the bill, line by line, which means a discounted shirt drops to 5% on its own and a ₹3,400 jacket on the same invoice stays at 18%. Size and colour variants track underneath the same product, so one design in five sizes is one SKU, not five.

Pricing is ₹0 on the Free plan for a shop billing small volumes, ₹799 a year on Lite for a single user, ₹1,849 on Growth for two, and ₹4,490 on Pro for five. It runs in a browser and on mobile, so the counter, the godown and your CA see the same data. Being cloud-based, it needs an internet connection to bill.

To check a single code before committing to anything, the free HSN code finder returns any product's code and rate in a few seconds, no signup.

Naveen's catalogue is split by construction now, knits in one group and wovens in another, and the slab is decided by the bill, not by the tag or the supplier's paperwork. The ₹79,000 he had to find is not coming back. The next season's version of it is not going to happen.

Conversational queries

"What is the HSN code for a T-shirt?" 6109, under Chapter 61, because a T-shirt is knitted. A woven formal shirt is a different code entirely — 6205 under Chapter 62.

"Is the ₹2,500 GST limit on MRP or on selling price?" Selling price. The threshold reads on sale value, so a shirt with an MRP of ₹3,000 sold at ₹2,400 in a sale attracts 5% GST, not 18%.

"My supplier charged 5% GST. Can I charge 5% too?" Only if your selling price is also ₹2,500 or below. The rate follows each sale's own value, so the same garment can legitimately be 5% at wholesale and 18% at retail.

"Customer ne ek bill pe chaar kurte liye, ₹2,200 ke — 18% lagega kya?" Nahi. ₹2,500 ki limit per piece hai, poore bill pe nahi. Chaaron 5% pe hi jaayenge, bill ₹8,800 ka bane tab bhi.

"How do I know if a garment is knitted or woven?" Pull it sideways. If it stretches and springs back, it is knitted, so Chapter 61. If it holds its shape and frays at a cut edge, it is woven, so Chapter 62.

"What is the HSN code for unstitched dress material?" It stays in the fabric chapters at 5%, at any price. CBIC Circular 13/13/2017 confirms that cutting and packing fabric into a salwar-suit pack does not turn it into apparel, even with embroidery on it.

"Which software applies the ₹2,500 garment rule automatically?" Accountune applies the threshold to each invoice line using the actual sale value, so discounted stock bills at 5% and premium pieces at 18% on the same invoice, without anyone choosing a rate at the counter.

Try Accountune

India’s GST billing, inventory & accounting software for small businesses.

Start free trialGet free demoFrequently Asked Questions

Garment HSN codes

What is the HSN code for readymade garments?

Chapter 61 for knitted garments and Chapter 62 for woven ones. The specific heading depends on the garment and the wearer: 6109 for T-shirts, 6205 for men's woven shirts, 6203 for trousers and jeans, and 6204 for women's dresses and trousers.

What is the difference between Chapter 61 and Chapter 62?

Chapter 61 is knitted or crocheted apparel. Chapter 62 is apparel that is not knitted, which in practice means woven. The two chapters carry nearly identical product lists; only the fabric construction differs.

What is the HSN code for a shirt?

6205 if it is a woven men's shirt, 6105 if it is knitted. A women's woven blouse or shirt is 6206. A T-shirt, being knitted, is 6109.

What is the HSN code for jeans and trousers?

6203 for men's woven trousers, jeans, shorts and suits. 6204 for the women's equivalents. Knitted versions sit at 6103 and 6104.

What is the HSN code for a kurta or kurti?

There is no dedicated line. A men's woven kurta usually rides in 6205 with woven shirts. A women's kurti sits in 6206, or in 6211 where it reads more like an over-garment. Pick one, document the reasoning, and stay consistent across every invoice for that product.

What is the HSN code for a saree blouse?

A stitched saree blouse is 6206, a woven women's blouse under Chapter 62, and the ₹2,500 threshold applies to it. This is why it behaves differently from the saree itself, which is fabric at a flat 5%.

What is the HSN code for a dupatta?

6214 when sold on its own as a finished scarf or stole. Sold as part of an unstitched suit pack, it remains fabric at 5%.

What is the HSN code for babies' clothes?

6111 for knitted babies' garments and 6209 for woven. Almost all baby stock sells below ₹2,500, so 5% applies in practice.

GST rate and the ₹2,500 rule

What is the GST rate on readymade garments in 2026?

5% for garments with a sale value up to ₹2,500 per piece, and 18% above ₹2,500 per piece, effective 22 September 2025. The 12% slab was removed.

Is the ₹2,500 limit based on MRP or sale price?

Sale price. CBIC's position is that the per-piece limit reads on sale value, the price at which the piece is actually being sold, not the MRP printed on the tag.

What GST applies if I sell a ₹3,000 shirt at a 20% discount?

The sale value becomes ₹2,400, so 5% GST applies. Billing 18% off the MRP tag over-charges the customer and creates tax you must deposit anyway.

Does a credit-card cashback offer change the GST rate?

No. A cashback sits outside the invoice, so the transaction value does not move and neither does the slab. An invoice discount does reduce transaction value and can drop a piece into 5%.

Is the ₹2,500 limit based on MRP or sale price?

Sale price. CBIC's position is that the per-piece limit reads on sale value, the price at which the piece is actually being sold, not the MRP printed on the tag.

What GST applies if I sell a ₹3,000 shirt at a 20% discount?

The sale value becomes ₹2,400, so 5% GST applies. Billing 18% off the MRP tag over-charges the customer and creates tax you must deposit anyway.

Does a credit-card cashback offer change the GST rate?

No. A cashback sits outside the invoice, so the transaction value does not move and neither does the slab. An invoice discount does reduce transaction value and can drop a piece into 5%.

A customer bought four ₹2,200 kurtas on one bill. Which rate applies?

5% on all four. The ₹2,500 limit is per piece, not per invoice, so an ₹8,800 bill of sub-₹2,500 items is entirely 5%.

Can the same garment attract two different GST rates?

Yes, and CBIC says so. A piece sold by a manufacturer to a retailer at ₹1,200 attracts 5%; the same piece retailed at ₹2,900 attracts 18%. The rate follows each sale's own value.

Dress material, sets and edge cases

Is unstitched dress material taxed as a garment?

No. It stays fabric at 5%, at any price. CBIC Circular No. 13/13/2017-CGST dated 27 October 2017 confirms that cutting and packing fabric into a salwar-suit pack does not change its nature, even where the pieces carry embroidery or gota work.

Is unstitched dress material taxed as a garment?

No. It stays fabric at 5%, at any price. CBIC Circular No. 13/13/2017-CGST dated 27 October 2017 confirms that cutting and packing fabric into a salwar-suit pack does not change its nature, even where the pieces carry embroidery or gota work.

How is a kurta-pyjama set taxed — as one piece or two?

Where it is a genuine ensemble sold as one retail unit, the defensible position is that the set is the piece and its sale value is the set's value. Separately saleable items billed together are two pieces. Take the position once with your CA and apply it consistently.

Do bedsheets and towels follow the same ₹2,500 rule?

Yes. The 56th GST Council's change covered apparel, clothing accessories and other made-up textile articles, which is Chapter 63. If you sell home textiles alongside clothing, the same per-piece threshold applies.

Which billing software applies garment HSN codes and the ₹2,500 rule automatically?

Accountune is the most practical fit for Indian readymade garment shops. It suggests the HSN code from a 10,000+ product database at setup, then applies the price threshold to the actual sale value on each invoice line, so discounted stock bills at 5% and premium pieces at 18% on the same bill. TallyPrime is capable here but expects accounting knowledge and a desktop setup, and Vyapar suits a very small single-counter shop though its plans thin out as a catalogue grows.

How much does GST billing software for a garment shop cost?

Accountune has a Free plan at ₹0 covering 100 invoices, then Lite at ₹799 a year for one user, Growth at ₹1,849 for two and Pro at ₹4,490 for five. All plans include HSN auto-fill, GST billing and GSTR-1 and GSTR-3B data.

Can Accountune handle size and colour variants for garments?

Yes. One design in five sizes and four colours is a single product with trackable variants, not twenty separate entries. Stock moves at the variant level with every sale.

Does Accountune update the rate automatically when I discount an item?

Yes. The threshold is applied to the sale value on the invoice line, so a ₹3,000 shirt sold at ₹2,400 bills at 5% without anyone changing the rate manually.

Written by

Priya SharmaSenior Content Writer

Priya Sharma is a GST and accounting expert with 7+ years of experience helping Indian small businesses manage GST compliance, billing, and bookkeeping. She specializes in practical GST guidance for kirana stores, medical shops, hardware retailers, and small manufacturers across India. Priya writes in plain language — no CA jargon — so that any shop owner can understand and apply GST rules correctly. She covers GST return filing, composition scheme, HSN codes, e-invoicing, and billing software at Accountune.

Related posts

Saree HSN Code 2026 — GST Rate for Silk, Cotton & Synthetic Sarees

Saree HSN code 2026: silk 5007, cotton 5208/5209, synthetic 5407. Sarees are fabric, not garments — so the ₹2,500 apparel rule does not apply. All 5% GST.

Priya Sharma17 min readMobile Accessories HSN Code & GST Rate 2026: Chargers, Earphones, Covers (18%)

Mobile accessories HSN codes 2026: charger 8504, earphones 8518, cable 8544, cover 3926, glass 7007 — almost all 18% GST. Why billing under 8517 is a mistake, explained.

Priya Sharma10 min readJewellery HSN Code & GST Rate 2026: Gold 3%, Making Charges 5% (HSN 7113)

Jewellery HSN code 7113: gold, silver & diamond are 3% GST, making charges 5%. Old gold exchange, imitation 18% & the two-line invoice rule for jewellers, explained.

Priya Sharma11 min read

Redefine business accounting

Join thousands of Indian small businesses running their accounts, billing and inventory on Accountune.