GSTR-1 vs GSTR-3B — Difference, Due Dates and Complete Filing Guide 2026

What is the difference between GSTR-1 and GSTR-3B? Due dates, Rule 88C mismatch rules, QRMP scheme — complete 2026 filing guide for Indian small businesses.

Reviewed by Accountune Compliance Team

On this page (32)

A Story That Thousands of Business Owners Will Recognise

Suresh runs a readymade garment shop in Jaipur. Three years of GST registration. A CA who handles the filings. Everything seemed fine — until February 2026 when a notice landed on his GST portal. Form DRC-01B. The message: your GSTR-1 shows higher tax liability than what you paid in GSTR-3B. Respond within 7 days.

His CA was travelling. The portal said 7 days — not 7 working days, 7 calendar days. Suresh searched online: ‘What is the difference between GSTR-1 and GSTR-3B?’ And he realised something uncomfortable. He had been filing returns for three years without fully understanding what he was filing or why.

That is not a failure on Suresh’s part. Most small business owners in India are in exactly the same position. Someone files on their behalf and the system runs quietly — until it does not. When a mismatch notice arrives, the lack of basic understanding turns a manageable compliance issue into a week of panic.

This blog explains exactly what GSTR-1 and GSTR-3B are, why both exist, how they are different, what their due dates are in 2026, what happens when they do not match, and how to keep your GST compliance clean without depending entirely on your CA for explanations. No jargon. No unnecessary complexity. Just what you actually need to know.

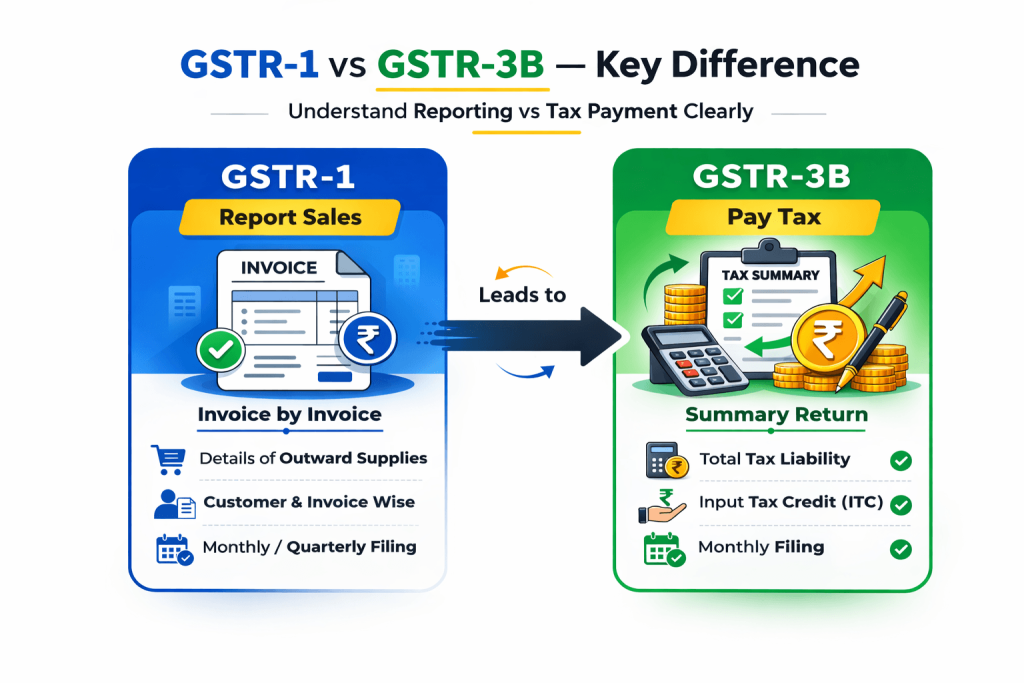

Quick Answer: GSTR-1 is a detailed invoice-by-invoice report of your sales — no tax is paid here. GSTR-3B is a summary return where you actually pay GST to the government and claim your Input Tax Credit. GSTR-1 is filed first, GSTR-3B is filed after. Both are mandatory for all regular GST-registered businesses.

Why Most Business Owners Get Confused Between the Two

The confusion is completely understandable. Both GSTR-1 and GSTR-3B contain sales figures. Both are filed monthly or quarterly. Both are related to GST. On the surface, they look like two versions of the same form.

The reality is that they serve completely different purposes in the GST system. One is a sales recorder. The other is a tax settler. Both need to match each other — and when they do not, the consequences in 2026 are more immediate than they used to be.

Before Rule 88C came into effect, mismatches between GSTR-1 and GSTR-3B were often caught manually or with a delay. Now the GST portal tracks them automatically. The moment your GSTR-1 shows higher tax liability than what you paid in GSTR-3B, the system generates a DRC-01B notice without any officer needing to intervene. Seven days to respond. No extensions by default.

2026 Critical Update: If you fail to file GSTR-3B for a previous period, the GST portal will block you from filing GSTR-1 for the current period. This directly affects your buyers — they cannot claim Input Tax Credit on your invoices. A single missed GSTR-3B can damage supplier-buyer relationships immediately.

Understanding why these two returns exist and what each one actually does is no longer optional knowledge. It is basic business literacy for any GST-registered operation in India.

What is GSTR-1 — Your Invoice-by-Invoice Sales Report

Think of GSTR-1 as your official sales diary submitted to the government. Every invoice you raised during the month, every B2B transaction with a registered business, every B2C sale above Rs 2.5 lakh for interstate transactions, every credit note and debit note — all of it goes into GSTR-1.

The most important thing to understand about GSTR-1 is what it does for your buyers. When you file your GSTR-1 and upload your B2B invoices, those invoices appear in your buyer’s GSTR-2B. That is how they get their Input Tax Credit. You delay filing GSTR-1 or skip an invoice — your buyer does not get their ITC for that period. Their working capital gets affected. This is why GSTR-1 filing on time is not just your compliance responsibility — it directly impacts your business relationships.

What Goes Into GSTR-1?

B2B invoices — every invoice raised to a GST-registered business, with their GSTIN

B2C sales — sales to unregistered customers (interstate sales above Rs 2.5 lakh shown separately)

Export invoices — goods and services exported with or without payment of tax

Credit notes and debit notes — amendments to previously issued invoices

HSN summary — a summary of goods and services sold by HSN/SAC code

Advances received — if you received advance payment before delivering goods or services

No tax is paid when filing GSTR-1. It is purely a reporting exercise. The government uses it to verify transactions, enable ITC flow across the supply chain, and cross-check with what you declare in GSTR-3B.

How Often Is GSTR-1 Filed?

If your annual turnover exceeds Rs 5 crore — you file monthly, due on the 11th of the following month. If your turnover is Rs 5 crore or below — you have the option to file quarterly under the QRMP scheme, due on the 13th of the month after the quarter ends. We cover QRMP in detail in a separate section below.

What is GSTR-3B — Where the Tax Actually Gets Paid

GSTR-3B is where money moves. While GSTR-1 is about reporting, GSTR-3B is about settling your tax account with the government.

Unlike GSTR-1, GSTR-3B does not require invoice-level detail. You do not list individual bills here. You enter consolidated totals — total taxable sales, total IGST collected, total CGST, total SGST, total ITC available, ITC claimed, and the net tax payable after adjusting credits. One set of summary figures per period.

GSTR-3B cannot be filed without paying the tax first. The portal will not accept the return unless the tax liability is cleared. This makes GSTR-3B fundamentally different from GSTR-1. It is a self-declaration of your tax position and a payment of what you owe.

One more critical point: GSTR-3B cannot be revised once filed. If you made an error, you cannot go back and correct it. You have to adjust the mistake in the next period’s GSTR-3B. This is why accuracy before filing matters enormously.

What Goes Into GSTR-3B?

Summary of outward taxable supplies — total sales and total tax collected

Inward supplies liable to reverse charge — purchases where you pay the GST instead of your supplier

Eligible Input Tax Credit claimed — ITC from your purchases, verified against GSTR-2B

ITC reversal — credits that need to be returned due to ineligibility

Net tax liability — output tax minus eligible ITC

Actual tax payment — CGST, SGST, IGST paid through cash ledger or ITC ledger

Late fees and interest — auto-calculated by the portal if filing is delayed

GSTR-1 vs GSTR-3B — Side by Side Comparison

Here is every important difference between the two returns in one place. Keep this for reference.

GSTR-1 vs GSTR-3B — Complete Comparison 2026

Comparison Point | GSTR-1 | GSTR-3B |

|---|---|---|

Primary Purpose | Report sales in detail | Pay tax + claim Input Tax Credit |

Level of Detail | Invoice-by-invoice | Summary totals only |

Tax Payment Required? | ✗ No tax payment at all | ✓ Mandatory before filing |

ITC Can Be Claimed? | ✗ Not here | ✓ Claimed in this return |

Filing Sequence | Must be filed first | Filed after GSTR-1 |

Monthly Due Date | 11th of following month | 20th of following month |

QRMP Due Date | 13th after quarter end | 22nd or 24th after quarter end |

Can It Be Revised? | Yes — amendment in next period | No — adjust in next return only |

Impact on Your Buyers | Feeds buyer’s GSTR-2B for ITC | No direct impact on buyers |

Late Fee (Normal) | Rs 50 per day (max Rs 10,000) | Rs 50 per day + 18% interest on tax |

Late Fee (Nil Return) | Rs 20 per day | Rs 20 per day |

2026 Blocking Rule | Blocked if previous GSTR-3B unfiled | Blocked if GSTR-1 mismatch unresolved |

The simplest way to remember this: GSTR-1 says ‘Here is what I sold.’ GSTR-3B says ‘Here is the tax I owe — take it.’

Which One Do You File First — The Correct Sequence

This confuses a lot of people. Some think it does not matter which you file first. It does. There is a specific sequence and there are real consequences to getting it wrong.

File GSTR-1 first — upload all your outward supply invoices for the month

Check GSTR-2B on the 14th — the portal auto-generates it based on your suppliers’ GSTR-1 filings. It shows exactly how much ITC you are eligible to claim

Reconcile GSTR-2B with your purchase records — is anything missing? If a supplier’s invoice is absent, contact them to file their GSTR-1

File GSTR-3B — claim only the ITC available in GSTR-2B, calculate net tax, pay and submit

This sequence exists for a reason. In 2026, under Section 16(2)(aa) being strictly enforced, provisional ITC is no longer permitted. You can only claim ITC that is actually reflected in your GSTR-2B. Claiming more than what GSTR-2B shows triggers a Rule 88D notice — a DRC-01C that requires you to either pay the excess back or explain.

Key Point for Buyers: Your ITC depends entirely on whether your supplier filed their GSTR-1. If a major supplier delays, your ITC gets delayed. This is why it makes sense to work with suppliers who have a clean GST compliance record.

GSTR-1 and GSTR-3B Due Dates for FY 2026-27 — Complete Calendar

These are the standard due dates for FY 2026-27. The government occasionally extends deadlines — always verify on the GST portal before assuming. Here are the dates you should plan around:

Monthly Filers — Turnover Above Rs 5 Crore

MONTHLY FILERS — TURNOVER ABOVE RS 5 CRORE

For the Month of | GSTR-1 Due Date | GSTR-3B Due Date |

|---|---|---|

April 2026 | 11 May 2026 | 20 May 2026 |

May 2026 | 11 June 2026 | 20 June 2026 |

June 2026 | 11 July 2026 | 20 July 2026 |

July 2026 | 11 August 2026 | 20 August 2026 |

August 2026 | 11 September 2026 | 20 September 2026 |

September 2026 | 11 October 2026 | 20 October 2026 |

October 2026 | 11 November 2026 | 20 November 2026 |

November 2026 | 11 December 2026 | 20 December 2026 |

December 2026 | 11 January 2027 | 20 January 2027 |

January 2027 | 11 February 2027 | 20 February 2027 |

February 2027 | 11 March 2027 | 20 March 2027 |

March 2027 | 11 April 2027 | 20 April 2027 |

QRMP Filers — Turnover Up to Rs 5 Crore

QRMP FILERS — TURNOVER UP TO RS 5 CRORE

Quarter | GSTR-1 Due Date | GSTR-3B Due Date | PMT-06 Monthly Payment |

|---|---|---|---|

Apr–Jun 2026 (Q1) | 13 July 2026 | 22/24 July 2026 | 25 May, 25 June |

Jul–Sep 2026 (Q2) | 13 Oct 2026 | 22/24 Oct 2026 | 25 Aug, 25 Sep |

Oct–Dec 2026 (Q3) | 13 Jan 2027 | 22/24 Jan 2027 | 25 Nov, 25 Dec |

Jan–Mar 2027 (Q4) | 13 Apr 2027 | 22/24 Apr 2027 | 25 Feb, 25 Mar |

Note on QRMP GSTR-3B dates: The 22nd deadline applies to Category 1 states and the 24th to Category 2 states. Check the GST portal to confirm which category your state falls under. The PMT-06 dates shown are for the first two months of each quarter — the third month’s tax is paid with the quarterly GSTR-3B.

The QRMP Scheme — What Businesses Under Rs 5 Crore Need to Know

QRMP stands for Quarterly Return Monthly Payment. It is a scheme designed specifically for businesses with annual turnover up to Rs 5 crore, and a large percentage of India’s GST-registered businesses qualify. Yet many business owners do not fully understand how it works.

Under QRMP, you file GSTR-1 and GSTR-3B once a quarter instead of every month. That is eight fewer return deadlines per year. The trade-off: you still pay tax every month through PMT-06. The government wants its money monthly, but it gives smaller businesses the convenience of quarterly paperwork.

The Invoice Furnishing Facility Under QRMP

IFF — Invoice Furnishing Facility — is an optional tool for QRMP taxpayers. If your B2B buyers need ITC urgently, they cannot wait until the end of the quarter for your GSTR-1 to be filed. IFF allows you to upload B2B invoices for the first two months of the quarter by the 13th of the following month. The last month’s invoices go into the actual quarterly GSTR-1.

Using IFF is not mandatory. But if you have buyers who regularly ask about ITC claims, using IFF in the first two months of each quarter makes you a more reliable supplier in their eyes.

Who Can Opt Into QRMP?

Annual turnover up to Rs 5 crore in the previous financial year or the current year

Must be a regular taxpayer or one who has opted out of the composition scheme

The last GSTR-3B return must be filed before opting in

Opt-in and opt-out windows open at the beginning of each quarter

Important: if your turnover crosses Rs 5 crore during any quarter of the current year, you become ineligible for QRMP from the next quarter and must shift to monthly filing. The GST portal adjusts this automatically.

What Happens When GSTR-1 and GSTR-3B Do Not Match — Rule 88C and DRC-01B

Let us come back to Suresh’s notice. The reason he received it was straightforward: his GSTR-1 declared a certain amount of tax from his sales, but the GSTR-3B for the same period showed a lower tax payment. The gap triggered an automated notice.

This used to be caught through manual scrutiny — which meant delays and inconsistency. Rule 88C, introduced in December 2022 and actively operational through 2026, automated the entire process.

How Rule 88C Works Step by Step

When your GSTR-1 tax liability exceeds your GSTR-3B tax payment by a threshold amount or percentage, the portal automatically generates Form GST DRC-01B. This appears on your GST portal dashboard and is emailed to your registered address. Part A of the form lists the mismatch — exactly how much the difference is.

From that moment, the clock starts. Seven calendar days.

You have two options within those seven days:

Pay the differential tax: Use Form GST DRC-03 to pay the shortfall along with 18% interest per annum calculated from the original due date. Then record the payment in Part B of Form DRC-01B.

Submit an explanation: If you believe the mismatch is due to a genuine reason — a timing difference, an amendment, a reporting error that did not affect actual tax payable — explain it clearly in Part B of DRC-01B with supporting documentation.

If neither option is exercised within seven days — no payment, no response — the portal blocks your GSTR-1 filing for subsequent periods. And recovery proceedings under Section 79 of the CGST Act can be initiated.

Seven days is not much time when your CA is busy or travelling. If you receive a DRC-01B notice, contact your tax advisor on the same day. Do not wait. The seven-day countdown does not pause for weekends or holidays.

Common Reasons for GSTR-1 vs GSTR-3B Mismatches

Reporting the correct invoice in GSTR-1 but entering it under the wrong table in GSTR-3B

Timing differences — a credit note issued after GSTR-1 was filed but before GSTR-3B

Incorrect tax head — paying CGST/SGST when the transaction required IGST or vice versa

Typos in tax amounts during manual data entry

Amendments to a previous GSTR-1 that were not reflected in the corresponding GSTR-3B

Duplicate invoices in GSTR-1 or missing invoices in GSTR-3B

Which GST Filing Tool Is Right for You

You can file GSTR-1 and GSTR-3B directly on the GST portal — it is free and requires no third-party tool. But if your business has more than 30 to 40 invoices per month, a purpose-built tool saves time and significantly reduces errors. Here are your realistic options:

GST Portal — Free and Manual

Filing directly on gstin.gov.in works perfectly well for very small businesses with a handful of invoices. It costs nothing. However, reconciliation between GSTR-1 and GSTR-2B has to be done manually, which takes time and introduces the risk of human error. For businesses with high invoice volumes, the manual approach is where mismatches originate.

ClearTax GST — Established Platform

ClearTax is one of India’s most widely used GST filing platforms, particularly among CA firms handling multiple clients. The GSTR-1 vs GSTR-3B comparison reports are detailed and useful. The pricing is on the higher side for individual small businesses. If your CA already uses ClearTax, staying on their platform makes sense.

Tally Prime — Desktop Accounting

Tally is deeply embedded in Indian accounting. If you already use Tally, it exports data for GSTR-1 and GSTR-3B filing. The limitation is that Tally is desktop-based — you cannot access it from your phone or from a different location. Multi-user access requires additional licensing and a local network. For businesses that work from a single office with a trained operator, it works. For flexible access and mobile visibility, it falls short.

Accountune — Cloud-Based for Small Businesses

Accountune is a cloud-based GST billing software and accounting platform built specifically for Indian small businesses. When you raise invoices through Accountune, GSTR-1 and GSTR-3B reports are automatically prepared based on your billing data. The reconciliation between your sales and tax figures is built in. There is no separate data entry step for returns — the billing data feeds the returns directly. It starts at Rs 799 per year and runs on mobile, tablet, or laptop without any installation. For business owners who are not accountants and do not want to become one, it is a practical fit.

Vyapar — Mobile-First Option

Vyapar is a popular billing app for small businesses at Rs 1,099 per year. Basic GST return reports are available. It works well for straightforward billing operations. The reconciliation features and accounting depth are limited compared to platforms designed specifically for compliance.

Honest Advice: No tool replaces understanding what you are filing. Whatever platform you use, spend 30 minutes understanding what GSTR-1 does and what GSTR-3B does. The tool makes it faster and more accurate — but the knowledge protects you when something goes wrong.

5 Practical Tips to Keep Your GST Filing Clean in 2026

Tip 1: File GSTR-1 by the 8th or 9th — Not on the Deadline

The due date is the 11th for monthly filers. But every month, thousands of businesses try to file on the 10th and 11th — and the portal slows down. Errors happen under time pressure. Get into the habit of filing GSTR-1 by the 8th or 9th. For QRMP filers, submit IFF invoices by the 10th to 12th. Your buyers will receive their ITC earlier and your compliance record stays clean.

Tip 2: Always Check GSTR-2B Before Filing GSTR-3B

GSTR-2B is available on the 14th of every month. Before you file GSTR-3B on the 20th, you have six days to review it. Match it against your actual purchase register. If a supplier’s invoice is missing from your GSTR-2B, contact them immediately — they need to file or correct their GSTR-1 before you can claim that ITC. Claiming ITC that is not in GSTR-2B is exactly the kind of issue that generates a Rule 88D notice.

Tip 3: Your GSTR-1 and GSTR-3B Tax Figures Must Match

If your GSTR-1 declares Rs 9.5 lakh in taxable sales with Rs 1.71 lakh in GST — your GSTR-3B should reflect the same taxable sales figure. Any deliberate or accidental difference is a mismatch that Rule 88C will flag. Genuine differences — such as a credit note — should be documented and handled correctly, not quietly adjusted in one return without the other knowing.

Tip 4: Set Monthly Reminders for the Entire Compliance Cycle

Create four phone reminders that repeat every month: 8th — file GSTR-1, 14th — check GSTR-2B, 18th — prepare GSTR-3B figures, 19th — file GSTR-3B. Following this cycle consistently means returns are never rushed and there is always time to catch and fix small errors before submission. One missed month makes the next month harder.

Tip 5: Respond to Any DRC-01B Notice Within 24 Hours of Receiving It

Not within seven days — within 24 hours of discovering it. Forward it to your CA immediately. Together, review the GSTR-1 and GSTR-3B figures for the flagged period. Identify whether the shortfall is a genuine tax underpayment or an explainable difference. If it is underpayment — pay through DRC-03 with interest and close it. If it is explainable — file a detailed explanation in Part B. The worst outcome is ignoring it because it seemed complicated. That leads to blocked returns and recovery action.

What You Should Take Away From This

Suresh resolved his DRC-01B notice. His CA submitted a Part B explanation — the mismatch was a genuine timing difference with a credit note. Case closed. But the seven days of stress, the calls, the uncertainty — all of it could have been avoided with basic familiarity with what these two returns do.

GSTR-1 and GSTR-3B are not complicated. One records your sales. The other pays your tax. They need to match. They need to be filed on time, in the right order, with accurate figures. That is the entire discipline.

In 2026, with Rule 88C making mismatch detection automatic, the stakes for getting this right are real. Not theoretical. Businesses that file accurately and consistently will not see DRC-01B notices. Businesses that treat returns as a formality handled by someone else — without understanding what is being filed — will eventually face exactly what Suresh faced.

Build a simple monthly cycle. File GSTR-1 by the 8th. Check GSTR-2B on the 14th. File GSTR-3B by the 19th. Use a billing tool that does the preparation work for you. Know enough to review what is submitted. That is all it takes.

If you are looking for a simple, cloud-based platform that automatically prepares GSTR-1 and GSTR-3B reports from your billing data — Accountune offers a 4-day free trial with no credit card required. Visit accountune.com to get started.

Try Accountune

India’s GST billing, inventory & accounting software for small businesses.

Start free trialGet free demoFrequently Asked Questions

General Questions

What is the main difference between GSTR-1 and GSTR-3B?

GSTR-1 is a detailed report of your sales — every invoice listed separately. No tax is paid when you file it. GSTR-3B is a summary return where you declare your total sales, claim Input Tax Credit, and actually pay your GST to the government. GSTR-1 is filed first; GSTR-3B is filed after.

Is it mandatory to file both GSTR-1 and GSTR-3B?

Yes. Both returns are mandatory for all regular GST-registered businesses. Even if there are no transactions in a particular month, you must file a nil return for both. Non-filing attracts late fees and damages your GST compliance rating on the portal.

Can I file GSTR-3B without filing GSTR-1?

Technically the portal may allow it in some cases, but you should never do this. Filing GSTR-3B without GSTR-1 creates a guaranteed mismatch. In 2026, under the current rules, failing to file GSTR-3B for a previous period blocks your GSTR-1 for the current period. The two returns are interdependent — treat them as a pair, always.

Which return should I file first — GSTR-1 or GSTR-3B?

Always file GSTR-1 first. After filing GSTR-1, check GSTR-2B on the 14th to verify your available Input Tax Credit. Only then file GSTR-3B with the reconciled figures. This sequence protects you from ITC mismatches and GSTR-1/GSTR-3B discrepancies.

Can GSTR-3B be revised after filing?

No. GSTR-3B cannot be revised once it has been submitted. If you made an error, you must adjust it in the next period’s GSTR-3B. This makes pre-filing verification critical — review your figures carefully before hitting submit.

Due Dates and Deadlines

What is the due date for GSTR-1 in 2026?

For monthly filers with turnover above Rs 5 crore, the GSTR-1 due date is the 11th of every following month. For QRMP filers with turnover up to Rs 5 crore, GSTR-1 is due on the 13th of the month after each quarter ends.

What is the due date for GSTR-3B in 2026?

Monthly filers must file GSTR-3B by the 20th of the following month. QRMP filers file quarterly — due on the 22nd for Category 1 states and the 24th for Category 2 states, in the month following the quarter’s end.

What is the late fee for GSTR-3B if I file after the deadline?

The late fee is Rs 50 per day per Act — Rs 25 under CGST and Rs 25 under SGST — up to a maximum of Rs 10,000 per return. For nil returns, it is Rs 20 per day. On top of the late fee, you also owe interest at 18% per annum on any unpaid tax, calculated from the original due date.

What happens if I miss the GSTR-1 due date?

A late fee of Rs 50 per day applies, up to Rs 10,000. More importantly, your buyers cannot claim ITC on your invoices for that period until you file. This delay affects their cash flow and can strain business relationships. GST compliance rating on the portal also suffers.

Is there a way to file GST returns with fewer deadlines?

Yes — the QRMP scheme allows businesses with turnover up to Rs 5 crore to file GSTR-1 and GSTR-3B quarterly instead of monthly. You still pay tax monthly through PMT-06 but the administrative burden of preparing and filing returns drops significantly. The IFF facility lets you share invoices with buyers monthly even under quarterly filing.

Mismatch and Rule 88C

What happens if GSTR-1 and GSTR-3B do not match?

Under Rule 88C, the GST portal automatically generates a Form DRC-01B notice when the tax declared in your GSTR-1 exceeds the tax paid in GSTR-3B by a defined threshold. You have 7 calendar days to either pay the differential tax with interest or submit an explanation. If you do neither, your GSTR-1 filing gets blocked for future periods.

What is Rule 88C in GST?

Rule 88C is a provision inserted in the CGST Rules in December 2022 that automates the detection of mismatches between GSTR-1 and GSTR-3B. When the tax payable as per GSTR-1 exceeds the tax actually paid in GSTR-3B by a specified amount or percentage, the portal sends an automated notice in Form DRC-01B without any manual intervention from a tax officer.

What is Form DRC-01B and what should I do if I receive one?

DRC-01B is the form through which the GST portal notifies you of a mismatch between your GSTR-1 tax liability and GSTR-3B tax payment. On receiving it, contact your CA or tax consultant the same day. Within 7 days, either pay the differential tax via DRC-03 with 18% interest or file a detailed explanation in Part B of DRC-01B explaining why the difference exists.

What are the most common reasons for GSTR-1 vs GSTR-3B mismatch?

The most common causes are entering the correct figures in GSTR-1 but placing them in the wrong table in GSTR-3B, timing differences with credit or debit notes, paying tax under the wrong head (IGST instead of CGST/SGST), typographical errors during data entry, and missing invoices in one return but not the other.

Can the GSTR-1 filing be blocked by the GST portal?

Yes, in two situations. First, if you have not filed GSTR-3B for the previous period, the portal will block GSTR-1 for the current period. Second, if you receive a DRC-01B notice and fail to respond within 7 days, the portal blocks future GSTR-1 filings under Rule 59(6)(d).

Input Tax Credit Questions

Can I claim ITC in GSTR-3B that is not in my GSTR-2B?

No. Under Section 16(2)(aa) being strictly enforced in 2026, provisional ITC is not allowed. You can only claim ITC that is reflected in your GSTR-2B. Claiming ITC beyond GSTR-2B triggers a Rule 88D notice via Form DRC-01C, requiring you to either reverse the excess or explain it within 7 days.

My supplier has not filed their GSTR-1 — when will I get my ITC?

You will receive the ITC in your GSTR-2B only after your supplier files their GSTR-1. This means you can only claim that ITC in the period when it appears in your GSTR-2B — which may be the following month or quarter. Encourage your regular suppliers to file GSTR-1 on time. Their compliance directly affects your working capital.

I accidentally claimed excess ITC in GSTR-3B — what should I do?

You should reverse the excess ITC in the next period’s GSTR-3B. If the excess is significant, it may attract interest. Self-correcting before a notice arrives is always the better outcome — a notice under Rule 88D carries additional pressure and the same 7-day response window.

Practical and Technical Questions

Can I file GSTR-1 and GSTR-3B myself without a CA?

Yes, absolutely. The GST portal allows any registered taxpayer to file their own returns. For businesses with simple transactions and a small number of invoices, self-filing is completely manageable. For businesses with multiple GST rates, B2B and B2C transactions, and significant ITC to reconcile, having a CA or a good GST-enabled billing software reduces the risk of errors significantly.

What is GSTR-2B and how is it different from GSTR-2A?

GSTR-2B is a static, auto-generated statement available on the 14th of each month. It shows the ITC you are eligible to claim based on your suppliers’ filed GSTR-1 data. It is static — it does not change after generation. GSTR-2A is a dynamic, real-time view of the same data that keeps updating as suppliers file. For ITC claims in GSTR-3B, GSTR-2B is the reference document in 2026.

How does GSTR-9 annual return relate to GSTR-1 and GSTR-3B?

GSTR-9 is the annual return filed by December 31 each year for the previous financial year. It consolidates all your GSTR-1 and GSTR-3B data across the year. If all your monthly returns were filed accurately and reconcile cleanly, GSTR-9 is straightforward. Mismatches in monthly returns accumulate and make annual filing complicated and potentially risky.

What is the penalty for a GSTR-1 vs GSTR-3B mismatch?

If it results in underpayment of tax, you owe interest at 18% per annum from the original due date. If a notice under Section 73 is issued and the tax is not paid within 30 days of that notice, a penalty of 10% of the tax amount or Rs 10,000 — whichever is higher — applies. Under Section 73(5), if you identify and pay the shortfall before receiving a notice, you only pay tax plus interest — no penalty.

Is GSTR-1 amendment possible after filing?

Yes. Errors in a filed GSTR-1 can be corrected through the amendment tables in the following period’s GSTR-1. You reference the original invoice and enter the corrected details. The amendment updates the buyer’s GSTR-2B for the period the amendment is filed. GSTR-1A is also available for corrections before GSTR-3B is filed for the same period.

I have two GST registrations in different states — do I file separate returns?

Yes. GSTR-1 and GSTR-3B must be filed separately for each GSTIN. You cannot combine returns across different state registrations. Each GSTIN has its own return filings, its own ITC pool, and its own compliance deadlines.

Does GST billing software actually reduce mismatch risk?

Significantly, yes. When your billing and GST return preparation happen in the same platform, the data is consistent by definition. Invoices you raise automatically feed into GSTR-1 report preparation. The same data goes into GSTR-3B. You review and submit — you do not re-enter. Manual re-entry is where most mismatches begin. Tools like Accountune, ClearTax, and others that integrate billing with return preparation eliminate that re-entry risk. The portal still requires a final review, but the numbers are already matched.

Written by

Priya SharmaSenior Content Writer

Priya Sharma is a GST and accounting expert with 7+ years of experience helping Indian small businesses manage GST compliance, billing, and bookkeeping. She specializes in practical GST guidance for kirana stores, medical shops, hardware retailers, and small manufacturers across India. Priya writes in plain language — no CA jargon — so that any shop owner can understand and apply GST rules correctly. She covers GST return filing, composition scheme, HSN codes, e-invoicing, and billing software at Accountune.

Related posts

Cement HSN Code & GST Rate 2026: 2523, 18% — Full Construction Materials List

Cement HSN code 2523 is 18% GST in 2026 (down from 28%). Full construction materials list — bricks, sand, steel, RMC, tiles — with HSN codes and rates for dealers.

Priya Sharma10 min readPaint HSN Code & GST Rate 2026 (3208/3209/3210) — 18%

Paint HSN code 2026: emulsion, enamel, distemper, primer, thinner & brushes with GST rates. Paint is 18% (down from 28%). Bill Asian Paints, Berger, Nerolac correctly.

Priya Sharma11 min readHSN Code List 2026: GST Rates for Every Common Indian Shop Product

Complete HSN code list 2026 with GST 2.0 rates (0/5/18/40%) for kirana, medical, hardware, electronics & garment shops. Find the right code, avoid penalties.

Priya Sharma2 min read

Redefine business accounting

Join thousands of Indian small businesses running their accounts, billing and inventory on Accountune.