What Is Input Tax Credit (ITC) in GST — Complete Guide 2026

What is Input Tax Credit in GST? Eligibility, Section 17(5) blocked credits, 180-day rule, GSTR-2B and how to claim ITC in GSTR-3B — complete 2026 guide.

Reviewed by Accountune Compliance Team

On this page (21)

The Rs 18,000 That Walked Out the Door

Ramesh owns a hardware store in Jaipur. Turnover of about Rs 1.2 crore a year. GST registered. Everything running smoothly — or so he thought. When his CA sat down with him at year end to review FY 2024-25, she asked a simple question: “Ramesh bhai, did you claim your Input Tax Credit on purchases?”

Ramesh had heard the term. He knew vaguely that it existed. But he had never asked his billing software to track it, never checked his GSTR-2B for eligible credits, and never claimed even a rupee of ITC across the full year. His CA ran the numbers.

Rs 18,000 in GST paid on purchases — eligible, available, and completely unclaimed. Gone. Not because there was a rule stopping him. Not because he was ineligible. Simply because he did not know how ITC worked or that he needed to actively claim it.

This story is not unusual. Thousands of small business owners across India — hardware dealers, garment shops, electronics stores, medical stores — pay GST on every purchase they make and let the credit sit unclaimed. This guide is going to fix that.

Wrapping Up — What ITC Means for Your Business

Ramesh eventually went back and recovered what he could within the allowed time limit. Not all of the Rs 18,000 — some invoices were past the deadline. But a significant portion was claimed and his monthly GST liability came down noticeably once he started tracking ITC properly.

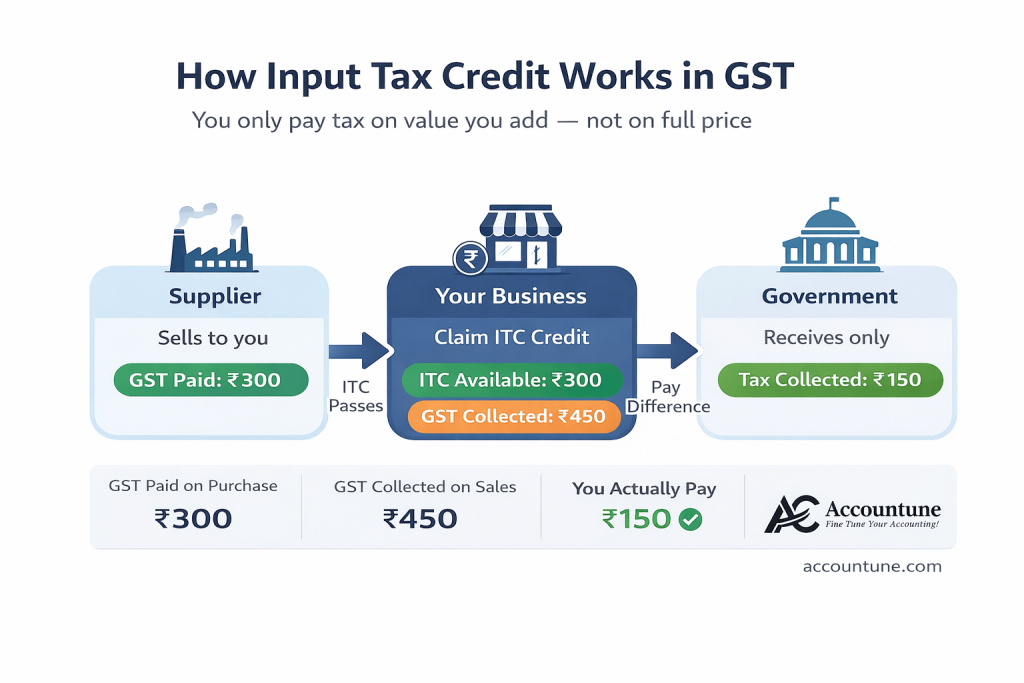

Input Tax Credit is not complicated once you understand the principle. You paid GST on what you bought. You collected GST on what you sold. The difference is what you owe the government.

The practical steps are simple. Check GSTR-2B on the 14th. Claim only what appears there. Pay your suppliers within 180 days. Do not claim blocked credits. File by the 20th. Do this every month and ITC takes care of itself.

If you are using Accountune for GST billing, your purchases are automatically reconciled against GSTR-2B. Every eligible credit is identified. Every missing invoice is flagged. Your GSTR-3B is pre-populated with the correct ITC figure — ready for review in minutes, not days.

|

Your Monthly ITC Workflow:

File GSTR-1 by the 11th (so your buyers’ GSTR-2B is correct)

Check your own GSTR-2B on the 14th

Match GSTR-2B with your purchase register — are all supplier invoices showing up?

If any invoice is missing — contact the supplier immediately

Claim only what GSTR-2B shows in your GSTR-3B

File GSTR-3B by the 20th

Accountune reconciles your purchase data against GSTR-2B automatically every month. Every eligible credit is identified. Every invoice missing from GSTR-2B is flagged before you file. Start free at accountune.com. |

In Short: In 2026, your eligible ITC is exactly what appears in GSTR-2B — generated on the 14th of every month. You cannot claim more than this.

What to Do When Your Supplier Did Not File GSTR-1

Your supplier issued you an invoice. You paid for the goods. You expect the ITC to show in your GSTR-2B on the 14th. It does not appear. Your supplier has not filed their GSTR-1.

Step-by-Step Action Plan:

Contact the supplier immediately. Call or WhatsApp. Many times the supplier simply forgot or is delayed. Give them until the 13th of the following month.

Check GSTR-2B the following month. If the supplier filed after the 13th cutoff, the invoice will appear in next month’s GSTR-2B.

Do not claim ITC that is not in GSTR-2B — no matter how certain you are. Claiming it anyway is a Rule 88D violation.

Use Rule 37A as your protection. Under Rule 37A, if your supplier fails to pay their GSTR-3B tax by September 30 of the following financial year, you must reverse the ITC — but you are protected from penalties if you acted in good faith.

For persistent non-compliance, reconsider the relationship. Every month their invoice is missing from your GSTR-2B is a month your cash flow is tighter than it should be.

In Short: Contact the supplier immediately. Wait for next month’s GSTR-2B. Do not claim the ITC until it appears. Document all follow-ups.

Last Date to Claim ITC in 2026 — The 30 November Rule

ITC cannot be claimed forever. There is a hard deadline — the earlier of: 30th November of the year following the financial year in which the invoice was issued, OR the date you file your annual return (GSTR-9).

Invoice Date | Last Date to Claim ITC |

April 2025 | 30 November 2025 |

September 2025 | 30 November 2025 |

March 2026 | 30 November 2026 |

April 2026 | 30 November 2026 |

September 2026 | 30 November 2026 |

March 2027 | 30 November 2027 |

Practical note: Since GSTR-3B for October is due on 20th November, the practical deadline is effectively 20th November.

In Short: All ITC for FY 2025-26 invoices must be claimed by 30 November 2026. Missing this deadline means the credit is permanently forfeited. Check old unclaimed invoices now.

How to Claim ITC in GSTR-3B — Step by Step

ITC is claimed in Section 4 of GSTR-3B — Table 4: Eligible ITC.

Log in to the GST portal at gst.gov.in with your credentials (GSTIN, username, password)

Go to Services > Returns > Returns Dashboard

Select the financial year and the return period (the month you are filing for)

Click Prepare Online for GSTR-3B

Navigate to Section 4 — Eligible ITC

Under Table 4A (ITC Available), enter the eligible ITC amounts from your GSTR-2B. Column (5): All other ITC — this is where most businesses enter their standard purchase ITC

Under Table 4B (ITC Reversed), enter any ITC you need to reverse — blocked credits, 180-day rule reversals, or partial use adjustments

Net ITC (4A minus 4B) is your eligible credit for the period

This net ITC is used to offset your output tax liability before any cash payment is required

Pay remaining liability, verify, submit, and file GSTR-3B using DSC or EVC

Important: ITC claimed in GSTR-3B must match GSTR-2B. The system now flags mismatches automatically.

ITC Reversal — When Do You Have to Give It Back

There are specific situations where you must return ITC you already claimed:

Reversal Situation 1 — 180-Day Payment Rule (Rule 37)

You claimed ITC but did not pay your supplier within 180 days. Reverse the ITC in the month when 180 days complete. Pay 18% interest from the original claim date. Re-claim when you actually pay.

Reversal Situation 2 — Blocked Credits Claimed by Mistake (Section 17(5))

You claimed ITC on a blocked item — office renovation, employee food, personal vehicle. Reverse it immediately in your next GSTR-3B. Interest at 18% per annum from the date of wrong claim.

Reversal Situation 3 — Goods Used for Both Business and Personal (Rule 42)

If purchases are used partly for business and partly for personal purposes — only the business portion qualifies for ITC. The personal portion must be reversed proportionally.

Reversal Situation 4 — Supplier Did Not Pay Tax (Rule 37A)

If your supplier filed GSTR-1 but failed to pay the actual GST in their GSTR-3B by September 30 of the following year — you must reverse that ITC.

Reversal Situation 5 — Goods Lost, Stolen, or Destroyed

If you claimed ITC on a purchase and those goods are subsequently lost in a fire, stolen, or damaged beyond use — the ITC must be reversed in the month the event occurs.

In Short: ITC reversal is mandatory in five main situations. Failure to reverse when required attracts 18% interest and penalties.

Billing Software and ITC — The Hidden Connection

Most small business owners do not realise that the accuracy of their ITC claims is directly tied to how their billing is done. The two are not separate.

Your billing software is where you raise invoices. Each invoice must have the correct HSN code, the correct GST rate, and the correct GSTIN of your customer. When your invoices are correct and filed in GSTR-1 on time — your buyers can claim their ITC from your invoices in their GSTR-2B.

On the purchase side — if your billing software tracks your purchase invoices, flags which ones are missing from GSTR-2B, and alerts you to unclaimed credits — you never miss ITC the way Ramesh did.

Accountune automatically matches your purchase data with GSTR-2B every month. Every eligible credit is identified. Every invoice missing from GSTR-2B is flagged. GSTR-3B is pre-populated with the correct ITC figure — ready for review and filing.

Try Accountune

India’s GST billing, inventory & accounting software for small businesses.

Start free trialGet free demoFrequently Asked Questions

General Questions

What is Input Tax Credit (ITC) in simple words?

ITC is the GST you paid on purchases that you can subtract from the GST you owe on sales. You pay tax only on the value you added, not on the full selling price.

Is ITC available for all GST-registered businesses?

No. Only regular GST taxpayers can claim ITC. Composition scheme taxpayers, businesses making only exempt supplies, and non-registered businesses cannot claim ITC.

What is the difference between input tax and input tax credit?

Input tax is the GST amount shown on your purchase invoices. Input tax credit is the mechanism that allows you to use that paid tax as a credit against your output tax liability.

Can ITC be claimed on both goods and services?

Yes. ITC can be claimed on GST paid for both goods and services purchased for business purposes, subject to eligibility conditions and blocked credit restrictions.

What documents are needed to claim ITC?

You need a valid tax invoice or debit note from a GST-registered supplier, proof that goods were received, and confirmation that the invoice appears in your GSTR-2B.

Eligibility Questions

Can a composition scheme dealer claim ITC?

No. Composition scheme dealers cannot claim any Input Tax Credit. The reduced flat tax rate is the trade-off for giving up ITC.

Generation Process

Can I claim ITC on my car purchased for office use?

No. GST on motor vehicles used for anything other than transportation of goods, passengers for hire, or driving training is blocked under Section 17(5).

Can I claim ITC on employee food and canteen expenses?

Food and beverages, outdoor catering, and similar services are blocked under Section 17(5) unless your business itself is a food service provider or the food is legally mandated.

Can I claim ITC on construction of my factory or office building?

No. Works contracts for construction of immovable property are blocked. ITC on machinery installed inside the building is available. ITC on the building itself is not.

Can I claim ITC on capital goods like machinery?

Yes. ITC on capital goods — machinery, equipment, computers, printers — is fully available in the year of purchase, provided the capital goods are used for taxable supplies and depreciation is not claimed on the GST component.

GSTR-2B and Supplier Questions

What is GSTR-2B and why is it important for ITC?

GSTR-2B is a static auto-generated statement available on the 14th of every month showing exactly which ITC you are eligible to claim. From January 2022, you can only claim ITC that appears in GSTR-2B.

What is the difference between GSTR-2A and GSTR-2B?

GSTR-2A is dynamic and updates in real time. GSTR-2B is static and generated on the 14th — it does not change after that date. For ITC claiming in 2026, GSTR-2B is the relevant document.

My supplier has not filed GSTR-1. Can I still claim ITC?

No. If the invoice does not appear in your GSTR-2B, you cannot claim ITC on it. Contact your supplier, ask them to file, and claim the ITC when it appears in a future GSTR-2B.

I paid a supplier who later stopped filing returns. What happens to my ITC?

Under Rule 37A, if your supplier fails to pay their GSTR-3B tax by September 30 of the following financial year, you must reverse the ITC you claimed on their invoices.

Can I claim ITC if my supplier issued a bill of supply instead of a tax invoice?

No. A bill of supply is issued for exempt supplies or by composition dealers who do not charge GST. Since there is no GST on a bill of supply, there is no ITC to claim.

Deadline and Timing Questions

What is the last date to claim ITC for FY 2025-26?

The last date is 30th November 2026 or the date of filing your GSTR-9 annual return for FY 2025-26 — whichever is earlier. The practical deadline is 20th November GSTR-3B filing.

Can I claim ITC for previous months if I missed it?

Yes, as long as you are within the November 30 deadline of the following financial year.

What is the 180-day rule for ITC?

If you claim ITC on a purchase invoice but do not pay the supplier within 180 days, you must reverse the ITC and pay 18% interest from the date of the original claim. Once you pay the supplier — even after 180 days — you can re-claim the ITC.

What happens to ITC if I file my GSTR-3B late?

You can still claim ITC in a late-filed GSTR-3B as long as you are within the November 30 deadline. You will owe late fees and interest on the tax portion but ITC itself is not lost by late filing.

Reversal Questions

When must I reverse ITC?

In five main situations — failure to pay the supplier in 180 days, claiming blocked credits under Section 17(5), partial personal use of business purchases, supplier failing to pay their GSTR-3B tax, and goods being lost, stolen, or destroyed.

What is the interest rate on wrongly claimed ITC?

The standard interest rate for ITC reversal is 18% per annum from the date of the wrong claim — whether for the 180-day rule, blocked credits, or any other reversal situation.

I accidentally claimed ITC on a blocked item. What should I do?

Reverse it immediately in your next GSTR-3B in Table 4B. Pay 18% interest from the date you originally claimed it. Self-correction before a notice avoids penalties.

Can I reclaim ITC after reversing it?

In some cases yes. If you reversed ITC because of the 180-day rule and then paid the supplier — you can re-claim the ITC in the period of payment. For blocked credits or goods lost — the ITC cannot be re-claimed.

Practical Questions

Can ITC be used to pay all GST liabilities?

ITC can be used to pay output tax (CGST, SGST, IGST). It cannot be used to pay interest, penalties, late fees, or any other dues. Those must be paid in cash.

Does billing software help in claiming ITC correctly?

Significantly yes. Good billing software reconciles your purchase invoices against GSTR-2B automatically, flags missing invoices, pre-populates GSTR-3B with the correct ITC figure, and tracks the 180-day payment deadline per invoice.

Written by

Priya SharmaSenior Content Writer

Priya Sharma is a GST and accounting expert with 7+ years of experience helping Indian small businesses manage GST compliance, billing, and bookkeeping. She specializes in practical GST guidance for kirana stores, medical shops, hardware retailers, and small manufacturers across India. Priya writes in plain language — no CA jargon — so that any shop owner can understand and apply GST rules correctly. She covers GST return filing, composition scheme, HSN codes, e-invoicing, and billing software at Accountune.

Related posts

7 Best Billing Software for Retail Shops in India 2026 -Tested & Compared

7 best billing software for retail shops in India 2026, compared on GST, inventory & price. Find the right fit for your kirana or medical shop.

Priya Sharma13 min read10 Best Invoice Software in India 2026 — Compared for Small Businesses, Freelancers and Retailers

Looking for the best invoice software in India? We compared 10 tools on price, GST features & ease of use. See which one fits your business.

Priya Sharma13 min readBest Free Accounting Software for Small Business in India (2026)

Five genuinely free options compared for Indian shops in 2026 — what each ₹0 plan actually includes, where the hidden limits sit, and which one fits your counter.

Priya Sharma9 min read

Redefine business accounting

Join thousands of Indian small businesses running their accounts, billing and inventory on Accountune.