GST New Rules from 1 April 2026 — The Complete Guide for Indian Small Business Owners

GST new rules April 2026 explained for Indian small businesses. ITC hard block, IMS, new rate slabs, e-invoicing — plain language. Free guide.

Reviewed by Accountune Compliance Team

On this page (18)

GST New Rules April 2026 have changed how Indian small businesses file returns, claim ITC, and generate invoices —

and most shop owners do not know it yet.

Suresh runs a hardware shop in Nagpur. Monthly billing around ₹8 lakh. GST registered, fairly regular with returns. Last Tuesday his CA called: “One of your main suppliers hasn’t been filing on time. From April 1, your GSTR-3B might get blocked.” Suresh had never heard of IMS. He had no idea what an ITC hard block was. He is not unusual. Across India, lakhs of shop owners are about to get hit by ten GST changes — and most of them do not know it yet.

From 1 April 2026, several GST rule changes come into full effect. Some began in September 2025 with the 56th GST Council meeting. Others are Budget 2026 amendments. Together, they change how ITC is claimed, how returns are filed, what rates apply to which goods, how bank details affect registration, and which businesses must now generate e-invoices. For small shops, kirana stores, wholesalers, and MSME owners across India, the compliance burden just got real.

This guide explains every change that matters — not the corporate version, not the CA-only version. The version that answers: what does this mean for my shop, and what do I need to do before April 1?

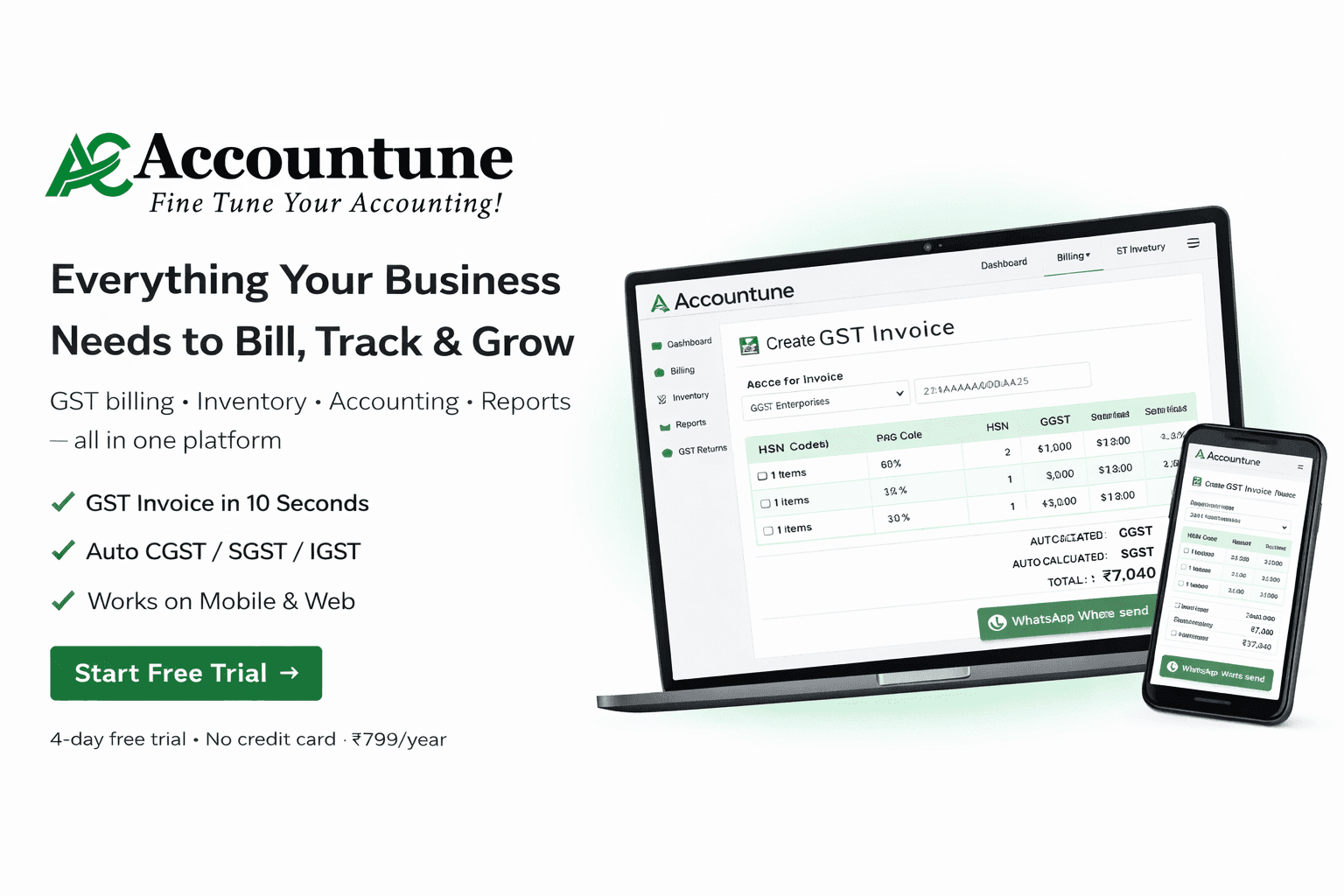

Accountune is cloud-based GST billing and accounting software built for Indian small businesses, starting at ₹799 per year. It automatically handles GSTR-1 and GSTR-3B data, purchase records for IMS reconciliation, and GST rate management — so the changes below are handled in the background while you run the shop.

1. What Is Changing from GST New Rules April 2026 — Overview

Ten changes. Each one has a different impact level depending on your business type.

Rule | Impact Level | Who Is Affected |

ITC Hard Block |  Critical | All GST-registered businesses |

Invoice Management System (IMS) | Critical | All GST-registered businesses |

GST 2.0 Rate Changes |  High | Businesses with 12% or 28% products |

GSTR-9 Annual Return | High | All registered taxpayers |

Post-Sale Discount Rule |  Medium | Businesses offering volume discounts |

Export Refund Threshold Removed |  Relief | MSME exporters, SEZ suppliers |

Intermediary Services = Exports | Major Relief | IT firms, consultants, agencies with overseas clients |

Bank Account Validation | Critical | All GST-registered businesses |

E-Invoicing ₹5 Crore Threshold | Critical | Businesses newly crossing ₹5 Cr in FY 2025-26 |

30-Day IRN Upload Rule | High | Businesses with AATO above ₹10 crore |

2. Rule 1: ITC Hard Block — The Biggest Change of April 2026

Until January 2026, the GST portal warned you when GSTR-2B and GSTR-3B showed different ITC amounts. A warning. Something you could note, plan to fix, and still file. That flexibility is ending. From April 2026, the warning becomes a wall.

What Is the ITC Hard Block?

If the Input Tax Credit in your GSTR-3B is higher than what GSTR-2B shows — based on what your suppliers have actually filed — the portal will not let you file GSTR-3B. Full stop. Zero Mismatch Policy is the official term. Your return stays blocked until you either reduce the ITC claim or wait for the supplier to file their returns.

What causes a mismatch? Your supplier filed late. Or with errors. Or not at all. In any case, their invoices raised for you do not appear in your GSTR-2B — meaning the ITC you paid on those purchases cannot be claimed, even though you paid the GST in good faith.

Important addition from December 2025: The portal also hard-blocks if RCM (Reverse Charge Mechanism) liabilities are unpaid, or if you have a negative balance in the Electronic Credit Reversal and Re-claimed Statement (ECRS). Both must be cleared before GSTR-3B opens for filing.

In short: From April 2026, GSTR-3B can only claim ITC that GSTR-2B actually reflects. No exceptions. One late-filing supplier blocks your entire return. Check supplier compliance monthly — before the 11th.

What this means for you: Log into the GST portal before the 7th of each month. Check which supplier invoices appear in GSTR-2B. Follow up with any supplier who is not appearing. Accountune’s purchase reports show supplier-wise purchase history — giving you a clean reference list for every reconciliation.

3. Rule 2: Invoice Management System (IMS) — Your New Weekly Compliance Task

IMS launched in October 2024 but was largely optional. From April 2026, because of the ITC hard block, IMS is effectively mandatory. The two rules work together — IMS is how you manage which invoices you accept, and the hard block is what happens if you accept too many.

How IMS Works

Every invoice your supplier raises for you appears in your IMS dashboard on the GST portal. You choose:

Accept — invoice is correct, goods received, ITC confirmed

Reject — wrong amount, wrong GSTIN, goods not received

Pending — decide later

Only accepted invoices flow into GSTR-2B as usable ITC.

New from October 2025: Bill of Entry (BoE) for imported goods — including imports from SEZ — is now also visible in IMS. If your business imports goods, you can take action on individual BoE records directly from IMS. This is a significant addition for importers and SEZ buyers.

Pending invoices depend on the supplier’s own filing — if they file, pending invoices get included in your GSTR-2B automatically. If they do not file, pending invoices drop out. Rejected invoices never appear, which means that ITC is permanently gone.

In short: Review IMS weekly. Accept correct invoices. Reject wrong ones promptly. Do not let the queue build. For importers — also review Bill of Entry records in IMS from October 2025 period onwards.

What this means for you: Accountune maintains a structured purchase ledger with invoice numbers, GSTINs, amounts, and tax breakdowns. When you sit down to work through IMS on the portal, your Accountune purchase records are the reference — not scattered paper invoices or WhatsApp messages from suppliers.

4. Rule 3: GST 2.0 Rate Rationalization — Check Your Products Before 1 April

The 56th GST Council meeting in September 2025 approved the most comprehensive GST rate overhaul since 2017. Effective 22 September 2025, and fully embedded in FY 2026-27 compliance from April 2026, the messy multi-slab structure is replaced by a cleaner one.

New Rate Structure — What Replaced What

Rate | Old Slab | Status | Examples |

0% | 0% | Unchanged | Unprocessed farm produce, public education, health/life insurance (new exempt) |

3% | 3% | Special rate — unchanged | Gold, silver, diamond, imitation jewellery (HSN 7113, 7117) |

5% | 5% / some 12% | Expanded | Basic medicines, packaged food, daily essentials, some healthcare equipment |

18% | 12% + 18% + 28% | Consolidated | Electronics, cement, steel, construction materials, most services |

40% | 28% + cess | New luxury slab | Luxury vehicles, luxury watches, tobacco, pan masala, aerated drinks |

Jewellery note: Gold, silver, and artificial/imitation jewellery remain at 3% GST under special rate provisions. HSN 7113 and HSN 7117 are both unaffected by the GST 2.0 changes.

Tobacco & cigarettes — special update: From February 2026, the GST Compensation Cess on tobacco products has been eliminated. In its place, tobacco and cigarettes are assigned new GST rates of either 18% or 40% depending on the product type, along with revamped Central Excise valuation mechanisms. Tobacco retailers and distributors must update their billing systems immediately to reflect correct rates — the old cess-based calculation is no longer valid.

In short: If any product in your billing software is set at 12% — update it to 18%. If any product is at 28% and is not a luxury item — update it to 18%. Accountune users can update item rates in the item master and the change applies to all future invoices immediately.

5. Rule 4: GSTR-9 Annual Return — Do Not Ignore This

From April 2026, the GSTR-9 (Annual Return) and GSTR-9C (Reconciliation Statement) for FY 2025-26 have auto-calculated late fees that increase daily. More critically, a pending FY 2025-26 annual return will block all FY 2026-27 monthly GSTR-3B filings on the portal.

Additionally, GST returns older than 3 years can no longer be filed. From January 2026, this cutoff is actively enforced. Any pending returns from FY 2022-23 or earlier — the ITC and reconciliation in them is permanently gone.

New from February 2026: The GST portal now auto-populates the “Tax Liability Breakup” section in GSTR-3B for any interest or tax liability from previous periods being discharged in the current return. Taxpayers must open this tab on the payment page and click “SAVE” before filing — otherwise the return may not submit correctly.

In short: File all pending annual returns before April 2026. Daily late fees are automatic. FY 2026-27 monthly filings are blocked if FY 2025-26 annual return is pending. And always click SAVE in the Tax Liability Breakup tab before submitting GSTR-3B from February 2026 onwards.

6. Rule 5: Post-Sale Discounts — Simpler But With New ITC Obligation

Earlier, a post-sale discount (volume discount, festival offer, year-end rebate) was only deductible from taxable GST value if there was a written agreement before the supply. Budget 2026 removed this prior-agreement requirement under Section 15.

However — there is a new obligation on the buyer side. Section 34 is now explicitly amended: when a supplier issues a credit note to reduce their tax liability, the recipient must reverse the corresponding ITC they had already claimed. This reversal must happen through IMS on the GST portal. If the recipient has not claimed ITC on the relevant invoice, no reversal is needed.

What this means in practice: Issuing a credit note is now simpler for the supplier — no prior agreement needed. But both supplier and buyer must ensure the ITC reversal happens correctly through IMS. Missed reversals on the buyer’s side can trigger compliance notices.

In short: Post-sale discounts from April 2026 — no prior written agreement needed. Issue credit note. Buyer reverses ITC through IMS. Both parties must coordinate. Accountune handles credit notes within the billing workflow, linked to original invoice with GST adjustment auto-calculated.

7. Rule 6: Export Refunds — No More Minimum Threshold

If your business exports goods or sells to SEZ units with payment of IGST, you were entitled to a refund — but only if the amount exceeded ₹1,000. Small MSME exporters with low-value orders lost out on small refunds that added up over the year.

From 1 April 2026, the ₹1,000 minimum threshold is removed. Any amount of IGST paid on exports is refundable. Additionally, inverted duty structure refunds now qualify for provisional refunds during final processing — improving cash flow while the full refund works through the system.

For exporters with a strong compliance track record (“Green Track” status on the portal), 90% of the refund amount is processed within 7 days of filing — down from the previous 14-day timeline.

In short: File refund claims for all IGST paid on exports — no amount is too small now. Accountune’s GST summary report shows IGST paid per transaction, making refund documentation clean and ready.

8. Rule 7: Intermediary Services — Zero GST for IT and Service Exporters

This is the single biggest relief in the April 2026 changes for service businesses. Previously, Indian companies providing services to overseas clients — IT firms, back-office operators, marketing agencies, consulting firms — were taxed at 18% GST even though the client was outside India.

From 1 April 2026, the place of supply shifts to the recipient’s location. If your client is in the US, UK, UAE, or anywhere outside India — your service now qualifies as an export of service. Zero GST. And you can claim ITC on all inputs used to deliver those services.

LUT reminder: To export services without paying GST, you must submit a Letter of Undertaking (LUT) for FY 2026-27. This should have been submitted by 31 March 2026. If not done yet, submit immediately — you cannot claim zero-rated status without a valid LUT for the current financial year.

Businesses that paid 18% GST on intermediary services in prior years should discuss retrospective refund eligibility with their CA.

In short: IT companies, consultants, and agencies serving overseas clients pay zero GST from April 2026. Submit LUT immediately if not done. Talk to your CA about retrospective refunds for prior periods.

9. Rule 8: Bank Account Validation — Easy to Miss, Very High Impact

This is the most overlooked rule of 2026. From January 2026, if a GST-registered business has not updated its bank account details on the GST portal, the system can automatically suspend the registration.

A suspended registration means:

You cannot file GST returns

You cannot generate E-Way Bills

Your buyers cannot claim ITC on your invoices

You cannot generate e-invoices

How to check: Log into the GST portal → My Profile → Bank Account Details. Verify that at least one active bank account with correct IFSC and account number is on record.

In short: Take 5 minutes right now. Log into the GST portal. Check that your bank account details are current and verified. This single task can prevent your entire GST registration from getting suspended.

10. Rule 9: E-Invoicing ₹5 Crore Threshold — Newly Covered Businesses

E-invoicing has been mandatory for larger businesses since 2020. From 1 April 2026, e-invoicing is mandatory for every business whose Aggregate Annual Turnover (AATO) crossed ₹5 crore in any financial year since FY 2017-18 — not just FY 2025-26.

This is the rule that catches most businesses off guard. If your turnover crossed ₹5 crore even once in any past year, e-invoicing applies to you right now — even if your current year turnover is lower.

This means:

Every B2B invoice must be uploaded to the Invoice Registration Portal (IRP)

IRP assigns a unique IRN (Invoice Reference Number)

IRN and QR code must appear on the printed invoice

Buyers cannot claim ITC on a B2B invoice without a valid IRN

If your business has GSTINs in multiple states, combined turnover of all GSTINs determines applicability

If you are not yet generating e-invoices and your turnover has ever crossed ₹5 crore — set it up immediately. Invoices issued without IRN are legally invalid for ITC purposes.

Accountune Growth and Pro plans include built-in e-invoicing. IRN is generated automatically when you create a B2B invoice — no separate portal login, no JSON upload required.

In short: If your FY 2025-26 turnover crossed ₹5 crore — e-invoicing is mandatory from April 1, 2026. Set it up before raising your first invoice of the new financial year.

11. Rule 10: 30-Day IRN Upload Rule — For ₹10 Crore+ Businesses

For businesses with AATO above ₹10 crore, a strict 30-day window applies for uploading invoices to the IRP. If an invoice is not uploaded within 30 days of the invoice date, the IRP permanently blocks IRN generation for that invoice.

This applies to invoices, credit notes, and debit notes. After the 30-day window closes, there is no workaround — the invoice cannot get an IRN, and the buyer loses ITC on it.

Practical impact: High-volume businesses with billing staff who process invoices in batches must implement same-day or next-day IRN generation as a standard process. Stacking invoices for end-of-month processing is no longer safe above ₹10 crore AATO.

In short: Above ₹10 crore AATO — generate IRN on every B2B invoice within 30 days of the invoice date. Build this into your daily billing process. Accountune generates IRN at the moment of invoice creation — no batch processing delay.

12. How Accountune Handles All 10 Changes Automatically

Most small business owners are not going to manually reconcile IMS every week, verify supplier filings before claiming ITC, update product rates across hundreds of SKUs, and track IRN deadlines. That is exactly what billing software exists to handle.

ITC Hard Block — Clean Purchase Records Ready Accountune records every purchase against a specific supplier with invoice number, GSTIN, amount, and GST breakdown. Your supplier-wise purchase report is the exact reference needed to check against GSTR-2B before filing GSTR-3B.

IMS Reconciliation — Organized Data, Not Chaos When you log into the GST portal to Accept or Reject invoices in IMS, your Accountune purchase ledger is the reference. Every invoice is recorded with date, supplier name, GSTIN, and tax amount — matching exactly what appears in IMS.

GST Rate Updates — Bulk Item Master Update Update any product rate in Accountune’s item master once — it applies to all future invoices immediately. No item-by-item updates at the counter. No risk of billing at the wrong rate after April 1.

GSTR-1 and GSTR-3B — Auto-Generated Every Month Every bill you create in Accountune feeds into GSTR-1 and GSTR-3B data automatically. At month end, your CA downloads the ready-format data. No manual compilation. No scramble. No calls asking you to send data at 10 PM on the 10th of the month.

E-Invoicing — IRN Auto-Generated at Billing Accountune Growth and Pro plans generate IRN automatically on every B2B invoice at the moment of creation. No separate portal login. No JSON upload. No 30-day deadline to chase. QR code and IRN print on the invoice automatically.

Credit Notes — Within the Billing Flow Post-sale discount? Issue a credit note in Accountune, link it to the original invoice, and the GST adjustment is calculated and reflected in reports automatically. Your CA can verify the ITC reversal obligation from the same report.

Unlike Tally, Accountune requires zero accounting knowledge to operate and starts at ₹799/year — not ₹22,500. Unlike Vyapar, Accountune works on web, Android, and iOS on every plan and includes CA remote login. Unlike myBillBook, Accountune includes e-invoicing and multi-location inventory on all plans.

[ CTA: See All Reports Live — Start Free Trial at app.accountune.com/auth/login ]

13. Accountune vs Vyapar vs Tally — GST Compliance GST New Rules April 2026

Feature | Accountune | Vyapar | Tally |

Starting Price | ₹799/year | ₹1,999/year | ₹22,500 license |

Platform | Web + Android + iOS | Android (desktop = extra plan) | Desktop only (cloud add-on) |

Auto GSTR-1 & 3B | Yes — auto-generated | Semi-automatic | Yes but needs trained staff |

E-Invoicing (₹5 Cr+) | All plans included | Higher plan only | Yes but complex setup |

CA Remote Login | Yes — all plans | Not available | Manual file sharing |

IMS-Ready Purchase Data | Clean auto-recorded ledger | Manual reconciliation | Possible but complex |

GST Rate Bulk Update | Yes — item master update | Item by item | Item by item |

30-Day IRN Auto-Generation | Yes — at billing moment | No | Manual process |

Credit Notes | Within billing flow | Available | Available but complex |

Accounting Knowledge Needed | Zero | Basic | High — trained staff required |

Free Trial | 4 days, no card | Limited free version | No free trial |

Competitor pricing sourced from public listings as of March 2026.

14. 7-Point Checklist — Do This Before 1 GST New Rules April 2026

Print this. Tick each one off.

1. Open your billing software item master. Find every product set at 12% GST — update to 18%. Find products at 28% that are not luxury goods — update to 18%. Save all changes before you raise the first April invoice.

2. Log into the GST portal. Go to IMS. Review the queue. Accept every correct supplier invoice. Reject any invoice with wrong amounts, wrong GSTIN, or goods you did not receive. If you import goods — also review Bill of Entry records. Do not leave the queue untouched.

3. Check your bank account details on the GST portal right now. Go to My Profile → Bank Account Details. If outdated or missing — update immediately to prevent automatic suspension of your GST registration. Also verify that Aadhaar authentication is completed on your profile — it is now mandatory for filing refund claims (RFD-01) and for revocation of cancelled GST registration. Without it, refund applications will be rejected by the portal.

4. Confirm that Multi-Factor Authentication (MFA) is active on your GST portal account. MFA is mandatory for all taxpayers from April 1, 2025. Without MFA, you may face session failures when generating e-invoices or e-way bills during peak filing periods.

5. Ask your CA: Is GSTR-9 for FY 2024-25 filed? Are there any returns older than 3 years pending? Clear all backlogs. Also confirm LUT is submitted for FY 2026-27 if you export services.

6. Make a list of your top 10 suppliers. Check if each one has been filing returns regularly. Any supplier who is consistently late will block your ITC from April 2026. Have a direct conversation or plan to stop claiming ITC from that supplier until they comply.

7. Check if your turnover has ever crossed ₹5 crore in any year since FY 2017-18. If yes — e-invoicing is mandatory for you right now, regardless of current year turnover. Set it up before your first April invoice. If above ₹10 crore — implement same-day IRN generation as a daily process GST New Rules April 2026.

8. If your business exports goods or services to clients outside India — call your CA today. You may qualify for zero GST on services and ITC on all inputs. You may also have a retrospective refund claim for GST paid on overseas client services before GST New Rules April 2026.

Try Accountune

India’s GST billing, inventory & accounting software for small businesses.

Start free trialGet free demoFrequently Asked Questions

General Questions

What are the main GST changes from 1 April 2026?

Ten major changes: ITC hard block on GSTR-3B, mandatory IMS (including BoE for importers), full GST 2.0 rate rationalization (0/5/18/40%), auto daily late fees on GSTR-9, simplified post-sale discount rules with mandatory ITC reversal, removal of export refund minimum threshold, intermediary services zero-rated exports, bank account validation causing auto-suspension, e-invoicing mandatory for ₹5 Cr+ businesses, and 30-day IRN upload rule for ₹10 Cr+ businesses.

Will 1 April 2026 GST changes affect my daily billing?

Yes — if any products you sell were at 12% or 28% GST. Those rates have changed. Update your item master before raising the first April invoice or you will be billing customers at a wrong rate, which creates GST filing mismatches and potential notices.

I am a small kirana store with 5-6 suppliers. Do these rules still apply to me?

Yes. If you are GST registered, the ITC hard block, IMS, and bank account validation apply to you regardless of business size. Even with 5 suppliers, if one does not file returns on time, your GSTR-3B gets blocked.

What happens if I do not make these changes before April 1?

You risk billing at wrong rates, losing ITC due to supplier filing mismatches, automatic GST registration suspension if bank details are outdated, and daily late fees on pending GSTR-9. Consequences compound — wrong rates → GSTR-1 mismatch → ITC blocked → returns stop filing.

What exactly is the ITC hard block?

A GST portal enforcement where GSTR-3B filing is blocked if ITC claimed exceeds GSTR-2B amounts. From December 2025, it also blocks if RCM liabilities are unpaid or ECRS balance is negative. Previously warnings — from April 2026, hard filing blocks with no workarounds.

My supplier is late with GST returns every month. What should I do?

Follow up immediately. From April 2026, their late filing directly blocks your ITC. Either stop claiming ITC on their invoices until they file, or find a more compliant supplier. Document follow-up in writing.

Can I still file GSTR-3B with partial ITC if some suppliers are non-compliant?

Yes. File GSTR-3B with only the ITC that GSTR-2B confirms. The hard block only prevents filing if you claim more than GSTR-2B shows. Recover remaining ITC in a later month once the supplier files.

Invoice Management System (IMS)

What is IMS and is it mandatory?

IMS — Invoice Management System — is the GST portal feature where you Accept, Reject, or mark Pending every supplier invoice. From April 2026, because of the ITC hard block, it is effectively mandatory. Bill of Entry for imported goods is also visible in IMS from October 2025.

What is IMS and is it mandatory?

IMS — Invoice Management System — is the GST portal feature where you Accept, Reject, or mark Pending every supplier invoice. From April 2026, because of the ITC hard block, it is effectively mandatory. Bill of Entry for imported goods is also visible in IMS from October 2025.

How often should I review IMS?

Weekly minimum. For high-volume businesses, twice a week is better. Never leave IMS unreviewed for a full month — the queue piles up and errors lead to over-claimed ITC (hard block) or under-claimed ITC (money lost).

If I reject an invoice in IMS, can I accept it later?

Yes, within the same return period. Once GSTR-3B is filed for that period, rejected invoices are permanently excluded from that period’s ITC.

GST Rate Changes

Which products moved from 12% to 18%?

Most goods in the 12% slab moved to 18% under GST 2.0 — including processed foods, textiles above a price threshold, non-essential household goods, and industrial inputs. Confirm against the 56th GST Council notification or ask your CA.

Is gold jewellery GST rate changing in April 2026?

No. Gold, silver, and imitation jewellery remain at 3% GST. HSN 7113 and HSN 7117 are both unaffected by the GST 2.0 rate changes.

What is now taxed at 40%?

The 40% luxury slab covers high-end automobiles, luxury watches, tobacco products, pan masala, and caffeinated aerated drinks. Tobacco cess eliminated from February 2026 — replaced with 18% or 40% GST depending on product.

What happens if my bank account is not updated on the GST portal?

From January 2026, the GST portal can automatically suspend your registration. Suspended registration means you cannot file returns, generate E-Way Bills, or issue valid e-invoices. Your buyers also lose ITC during suspension.

How do I update bank account details on the GST portal?

Log into GST portal → My Profile → Bank Account Details → Add or update with correct IFSC and account number. Verification is automatic. Takes less than 5 minutes.

E-Invoicing

My business crossed ₹5 crore turnover. Is e-invoicing mandatory now?

Yes — and this applies to any year since FY 2017-18, not just the current year. If your AATO exceeded ₹5 crore in any past financial year, e-invoicing is mandatory right now. Accountune Growth and Pro plans include built-in e-invoicing — IRN generated automatically at billing.

What is the 30-day IRN upload rule?

Businesses with AATO above ₹10 crore must upload invoices to IRP within 30 days of invoice date. After 30 days, IRN generation is permanently blocked — no exceptions. Applies to invoices, credit notes, and debit notes.

Annual Returns and Filing

What is the GSTR-9 deadline and what happens if I miss it?

GSTR-9 for FY 2025-26 is due December 31, 2026. From April 2026, late fees are auto-calculated daily. Pending annual returns also block all FY 2026-27 monthly GSTR-3B filings.

I have not filed some returns from 2022-23. Can I still file them?

No. From January 2026, GST returns older than 3 years are permanently blocked. Returns for FY 2022-23 and earlier cannot be filed. ITC from those periods is permanently lost.

Credit Notes and Discounts

How does the new post-sale discount rule work from April 2026?

No prior written agreement needed. Issue a credit note. However — the buyer must explicitly reverse the proportionate ITC through IMS on GST portal. If buyer has not yet claimed ITC on that invoice, no reversal needed.

Exports and Refunds

What changed for GST export refunds?

The ₹1,000 minimum threshold for IGST-paid export refunds is removed. Any amount is now refundable. Exporters with strong compliance history receive 90% of refund within 7 days.

I provide IT services to a US client. Do I still pay 18% GST?

No — from 1 April 2026. Your service qualifies as an export. Zero GST applies. Submit a valid LUT for FY 2026-27. Without LUT, you must pay IGST and claim refund later.

What is LUT and do I need it?

LUT — Letter of Undertaking — lets you export without paying GST upfront. Submit fresh every financial year. For FY 2026-27, deadline was 31 March 2026. If not done — submit immediately.

Using Accountune for April 2026 Compliance

Does Accountune automatically update GST rates for my products?

Accountune applies whatever rate is set in your item master. Update once — all future invoices use the new rate automatically. No item-by-item updates, no wrong rate risk after April 1.

Which Accountune plan is right for my shop?

Lite — ₹799/year: 1 user, GST billing, inventory, GSTR reports, CA access. Growth — ₹1,849/year: 2 users, e-invoicing IRN, 2000 invoices, 300 E-Way Bills. Pro — ₹4,490/year: 5 users, 10,000 invoices, priority support, no branding on invoices. All plans include a 4-day free trial — no credit card required.

What does Accountune’s CA login include?

Dedicated CA login with access to GSTR-1 and GSTR-3B reports, purchase and sales ledgers, GST summaries. CA works independently without calling you. Included in all plans from ₹799/year.

Written by

Priya SharmaSenior Content Writer

Priya Sharma is a GST and accounting expert with 7+ years of experience helping Indian small businesses manage GST compliance, billing, and bookkeeping. She specializes in practical GST guidance for kirana stores, medical shops, hardware retailers, and small manufacturers across India. Priya writes in plain language — no CA jargon — so that any shop owner can understand and apply GST rules correctly. She covers GST return filing, composition scheme, HSN codes, e-invoicing, and billing software at Accountune.

Related posts

7 Best Billing Software for Retail Shops in India 2026 -Tested & Compared

7 best billing software for retail shops in India 2026, compared on GST, inventory & price. Find the right fit for your kirana or medical shop.

Priya Sharma13 min read10 Best Invoice Software in India 2026 — Compared for Small Businesses, Freelancers and Retailers

Looking for the best invoice software in India? We compared 10 tools on price, GST features & ease of use. See which one fits your business.

Priya Sharma13 min readBest Free Accounting Software for Small Business in India (2026)

Five genuinely free options compared for Indian shops in 2026 — what each ₹0 plan actually includes, where the hidden limits sit, and which one fits your counter.

Priya Sharma9 min read

Redefine business accounting

Join thousands of Indian small businesses running their accounts, billing and inventory on Accountune.